Open Banking & Bank APIs

Open Banking for Business

Imagine a world where your banks communicate seamlessly with all of your internal accounting, cash management, and other financial software. You’d save time by not having to manually download all of your transactions, reformat them, and then upload them somewhere else (database engineers call this process ETL, but your finance team calls it error-prone drudgery).

That world is already here. Faster, more accurate financial data is enabled through Open Banking.

What is open banking?

Simply put, open banking is about moving data about money from Point A (the banks) to Point B (your financial tools, where you actually need it). It leverages Bank APIs and other forms of data transfer to get your data where you want it — because you own your data, not the banks.

Much of the Fintech revolution has been driven by the concepts of open banking. The industry exploded onto the scene because it enabled personal banking options (nearly everyone uses a bank). Think Venmo, Plaid, and even Klarna, all run on open banking software.

But the revolutionary changes coming for open banking, including some that are already here, are happening on the commercial side of things. Businesses need better financial information so they can make better-informed and quicker decisions about what to do with their hard earned cash.

Why are companies leveraging open banking?

Whether you’re a startup looking for a competitive edge or you’re the treasurer at a Fortune 1000 company in need of a digital transformation to keep growing, open banking is the first step toward that critical cash visibility.

The business benefits of open banking

On the surface, the benefits of deploying automation for your bank data are simple: speed and accuracy. These two things alone make switching to automated workflows a no-brainer, but the benefits of open banking go much deeper than pushing a button and getting near-instant results compared to what used to take hours every day.

Streamline your payments

With bank APIs, you don’t just speed up how you ingest your data about transactions, you also speed up payments. Leveraging Real-Time Payments (RTP), ACH, and wire transfers all in one place, you can keep your cash working for you longer before you pay for your liabilities. Learn more about how open banking APIs simplify payment operations.

Understand how open banking and real-time payments can make a real difference in your organization:

Decide which payment system is right for your transactions

Learn how Open Banking APIs simplify payment operations

Discover how Trovata’s Payments App empowers businesses like yours

Listen to Trovata’s podcast Fintech Corner as they explore open banking for payments

Watch a previously-recorded webinar about payment acceleration with Trovata

Get real-time cash visibility

The incredible leap forward happens when you start using all of that bank data. Whether you’re preparing cash flow statements, daily cash positioning, or forecasting future cash flows, your fully-normalized data, all collected in one place, makes these finance tasks a breeze (or at least faster and more accurate).

Do more with your data

Unless you collect your data from your banks and warehouse it somewhere, you don’t really own it or get its full benefit. Some banks let you download the last 90 days of transactions. Others can go back as far as 24 months.

Tools which collect your bank data (and keep it private) let you keep it forever — like we do. This unlocks the power of your data in useful ways:

Get a single birds-eye view and deep-dive capabilities for your multi-bank data

Easily share your data with your other financial software tools, like ERPs

Perform historical analyses at the press of a button

Professional presentation of financial data to third parties (banks, investors, journalists, etc.)

Optimized risk management and cash management decision-making

In your first 30 days with Trovata, after our concierge team gets you all set up, open banking enables:

Reduce accounts payable timeline and complexity with RTP

Get accurate and fast reconciliation, on demand

Cash positioning updated all day long

After 30 days, the full benefits of Trovata kick in enabling cash forecasting, deeper analysis of spending, and historical analysis like MOM, HOH, and YOY comparisons. All of this is made possible with open banking and bank APIs.

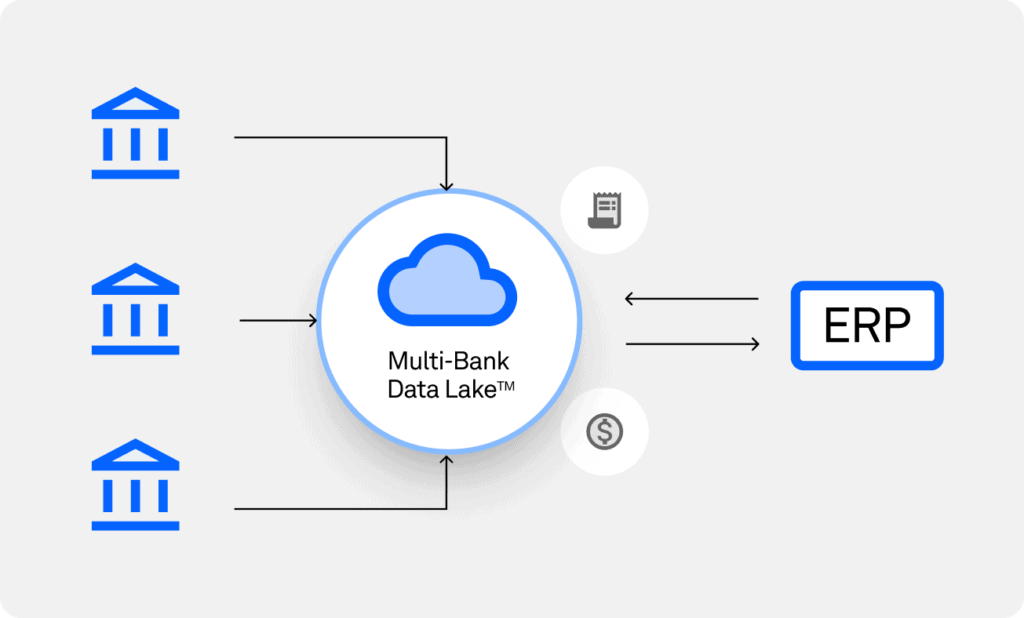

How open banking works at Trovata

At Trovata, all of our treasury management capabilities run on open bank data

The process works like this:

We automatically collect your financial data (or you can collect it on demand) from all your banks

We normalize this data and store it in our secure Multi-bank Data Lake

We provide tools to make use of that data for cash management, payments, and analysis

We make your data ready for, and hand it off to, other tools like ERPs and accounting software

The current open banking landscape at Trovata

This list of banks and integrations covers a wide swath of open banking opportunities, but the Trovata team is always working to add new banks and new third-party integrations. Where we can’t already meet your needs, your development team can build their own integrations with our custom, well-documented API.

Hit the ground running

After you sign up with Trovata, there are two parts to getting the power of open banking working for you. First, you’ll need to secure authorization from each of your banks for us to connect with their systems and gather your data.

Then, our onboarding team gets everything set up for you. The timeline for this process varies depending on your banks, the authorization timeline, and the complexity of their open banking setup.

Are Bank APIs and Bank Feeds the same thing?

Yes and no. It sort of depends on who you ask. Bank Feeds, a term coined by accounting software companies like Intuit and NetSuite, are a non-techie way to discuss connectivity between financial institutions and financial software.

Bank APIs are one kind of bank feed, but so are SWIFT and BAI. While we talk a lot about our Bank APIs, because we’re leading the way with API connectivity for treasury management, we leverage all manner of bank feeds to get your data to you.

Multi-banking is smart banking

Prior to the collapse of Silicon Valley Bank (SVB) and the few that followed, many companies were lax about keeping funds in single accounts in excess of the FDIC limit. Should your one bank have problems, as was the case for start-up BOXT who banked exclusively with SVB, your funds might be inaccessible for a period of time, jeopardizing all of your organization’s operations.

But multi-banking, while better for cash preservation, creates headaches of its own — how do you manage and visualize transactions across multiple banks all on one screen? This is one of Trovata’s key features — API-driven multi-bank cash reporting made easy. And it all relies on our Multi-Bank Data Lake

What is the Multi-bank Data Lake?

In order for API interoperability to be realized, the data needs to live somewhere in between operations. In the case of Trovata, this is our Multi-Bank Data Lake. Each client has a secure data lake of their own.

When data arrives via API, it must be normalized before it can be stored in our data lake. This normalization process is what takes data from disparate bank sources using their own terminologies and unifies all of your banks’ data into one common “language” which is understood by Trovata’s systems.

One of the best features of our Multi-bank Data Lake is that you can keep your data forever. Some banks only let you download the last 90 days of transactions, while others go back as far as 24 months. It’s your data, we think you should be able to access it when you need it.

Open banking security and safety

In this era of bad actors leveraging all of this data interoperability to their benefit, data security takes a front-and-center role when considering the shift to automated cash management. Let’s talk about the security of open banking in general, and specifically what Trovata does to make your data secure.

Security of your data at Trovata

Trovata is fully SOC1 Type 2 and SOC2 Type 2 certified. We post our certifications along with our monitoring scheme. We ask you to provide credentials to download the information in the reports to keep them more secure. Our third-party Security Scorecard rating is 98/100.

We actively (in real time) monitor: infrastructure security network security, data security, product security, app security, and organization security. We log every action performed in the system.

We perform monthly risk assessments to ensure the application is secure.

Companies who succeed with open banking

Open banking is revolutionizing cash management at mid-level enterprises up through the Fortune 50. Some of our favorite case studies about how open banking at Trovata changed a company's cash operations include Krispy Kreme and Eventbrite.

“When I first joined Eventbrite, my day-to-day consisted of logging on to all of our different bank portals, running reports to see balances for each of our accounts, and then trying to standardize all of this data in excel to build summaries. Then I had to do this across all four of our main banks. I spent 2-3 hours a day pulling and normalizing bank data before Trovata, and that wasn’t a good use of my time.”

“With Trovata, we have been able to automate daily, weekly, and monthly cash reporting. It has become our easy-to-use reconciliation tool for our Accounting team.”

– Niall Burke, Global Treasury Manager at Eventbrite

Read the Treasury Automation Eventbrite case study

“As treasurer, my role has to do with funding the business and optimizing its lifeblood; cash. Just like the human body needs good blood flow to stay healthy, a global enterprise needs proper cash flow. It’s vital we ensure proper flow and circulation of our cash.”

“Since we started using Trovata, our treasury technology capabilities have completely transformed for the better. We have more time to focus on driving strategy and unlocking growth opportunities.”

– James Krikorian VP & Treasurer at Krispy Kreme

Read the case study about Krispy Kreme API & Modern Cash Flow management

Subscribe to Newsletter

You May Be Interested In These Other Resources