The insurance business is one of the oldest in existence. The first known insurance contract can be traced back to 1347, and yet the industry is still changing rapidly almost 700 years later.

Many of the fundamental issues facing treasurers are the same that the European pioneers were dealing with hundreds of years ago, like managing liquidity and payout ratios.

But unlike underwriters in the 15th century, modern treasurers now need to deal with a wide range of additional complexities, such as the web of payments infrastructure and new trends in claims. Keeping up with these challenges requires modern tools to simplify insurance treasury management.

In this article, we’re going to cover some of the key challenges facing treasurers, CFOs and finance teams in the insurance industry, and explain how technology like Trovata is helping to solve them.

The Complexities of the Insurance Sector

Historically, the insurance business has been relatively stable and consistent. Over time, actuaries have become highly skilled at assessing risk, aided by a very long history of claims data. But as the last couple of decades has shown us, the internet age has thrown much of that traditional wisdom out the window.

Here are some of the key challenges facing insurance treasurers today.

Payments and Transaction Volume

One of the biggest changes has been the way payments are made. Reconciliation has become a major issue, with customers now able to pay for their policies through an eye watering array of methods.

Of course you still have traditional payment sources such as electronic transfers and credit cards, but insurers also need the ability to reconcile payments from services like Stripe and WePay, as well as accepting financed annual premiums and dealing with an ever-increasing number of micro transactions providing cover for anything from concert tickets to weddings.

Keeping track of all this and getting bank reconciliation right, particularly for global insurers, is a challenge that is only getting more complex with every passing year.

Fraud and Scams

Unfortunately, rates of insurance fraud have increased exponentially since the birth of the internet. Back in 1995, insurance fraud was estimated to be around $80 billion (around $160 million today when adjusted for inflation). Now, that figure has rocketed up to an estimated $308 billion.

That creates challenges on both fronts. Not only do insurers need to be hyper-vigilant in ensuring they limit the impact of fraud and scams, but treasurers also need to plan for the associated costs in their forecasts and cash management plans.

Increasing Liquidity Focus

Liquidity hasn’t always been a major concern for insurers. With the right calculations on probabilities and costs and premiums paid upfront, the business has traditionally been fairly predictable.

But the 2008 global financial crisis was a stark reminder that this isn’t always the case. The mispricing of assets in the housing market led to a massive failure at AIG, which required a government bailout of $150 billion.

The subsequent regulatory changes off the back of the crash has also had an impact on the industry, with stricter guidelines around liquidity requirements for individual policies and business units, meaning that liquidity can’t just be managed at a company level.

Treasurers need to ensure their overall cash position is strong, but also that they are meeting legal liquidity requirements across every section of the business.

Not only that, but the subsequent zero interest rate policy had substantial impacts on the bond markets, making it much more difficult for insurers to find attractive yields without significantly increasing their risk.

As mentioned in a recent note from EY, insurers must increasingly rely on technology to manage their liquidity position, with internal stress testing and robust cash flow forecasts more important than ever.

New Forecast Challenges

Speaking of which, it’s not just the financial environment which is making forecasting more difficult. The claims landscape has also changed substantially. Health insurers in particular are facing a tidal wave of additional payouts due to social changes related to mental health in particular.

The publicity around mental health has moved it into the mainstream, with claims for conditions such as anxiety and depression climbing dramatically. According to data from Swiss Re, the total cost of mental health related issues accounted for 20.5% of total payouts in 2015, but this figure had risen to 39.8% by 2020.

At the same time we have demographic changes, new technology such as key cloning creating an increase in car thefts, increased competition in the insurance sector and heightened regulatory scrutiny.

All that is to say that an industry which has always been fairly predictable, now isn’t quite so much. That makes cash flow forecasting substantially more difficult (and important) for treasurers.

The New Tech Innovations Changing Insurance Cash Management

But the good news is that technology is helping to deal with a lot of these challenges. Specifically, there are three main tech innovations that are serving as the back end for modern cash management solutions like Trovata, helping treasurers see more and do more, in far less time.

1. Cloud native platforms

Collaboration has never been more important in the insurance sector. Teams are globally dispersed, and multiple departments need the ability to work together, from claims to sales to underwriting and customer service.

The problem has always been a wide variety of software and spreadsheets that have been used to run each different department. This makes collaboration incredibly challenging, as well as increasing risk to the business through proliferation of manual inputs and models.

To improve efficiency in a business that works with massive amounts of data, is to make sure that every team has access to it. Sounds obvious, but even today, many insurance companies rely heavily on a mix of Excel spreadsheets and cumbersome, dated software which is siloed from other parts of the company.

Moving to a cloud based software solution not only means better collaboration, but also reduced risk. Data security is drastically improved when all your team is using a single source of truth for all of their financial information.

There no longer needs to be a concern about a spreadsheet file being accidentally emailed to the wrong person, or an outdated version being sent to an executive to base their corporate strategy on.

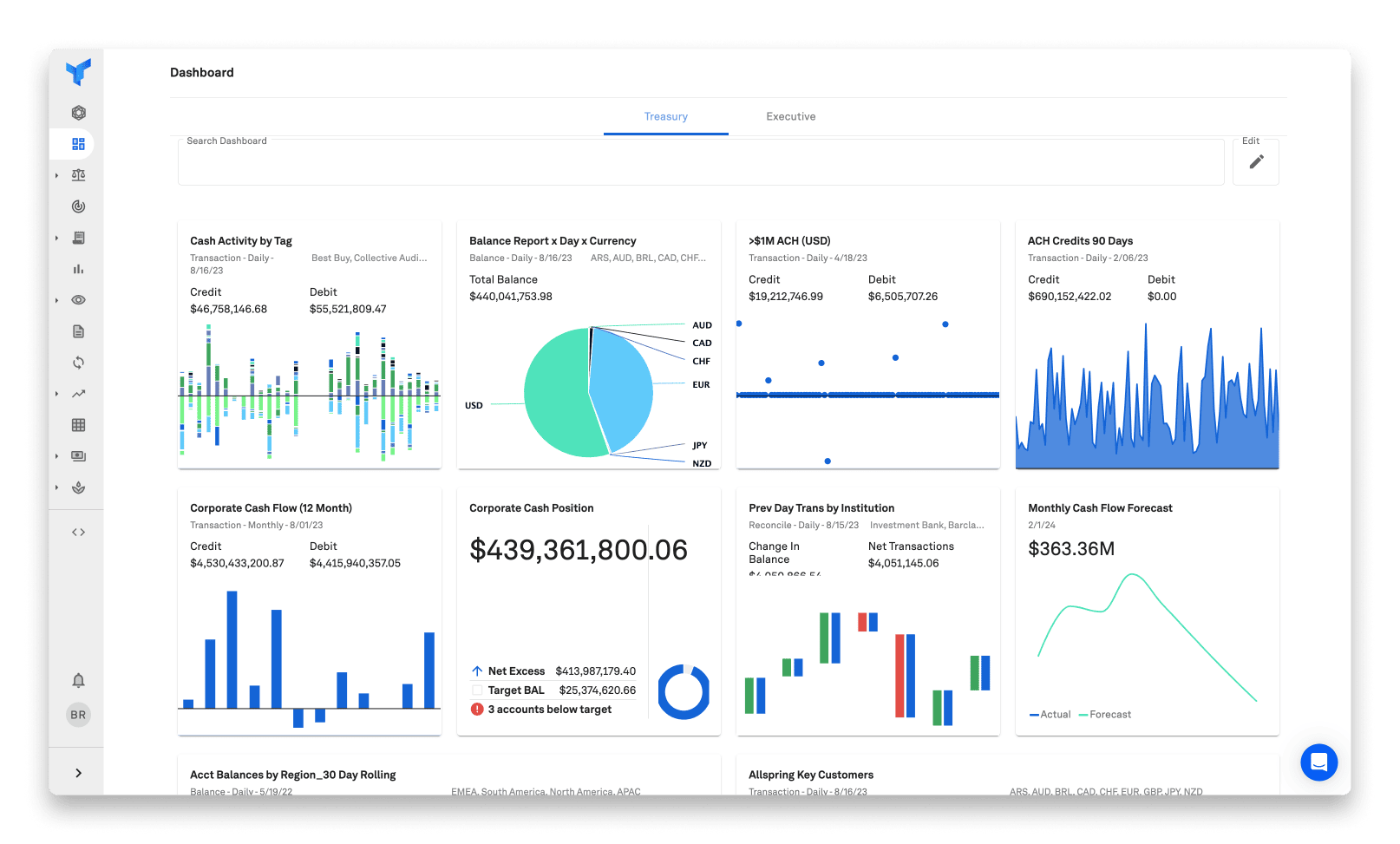

When you use Trovata, everyone has access to the same single source of truth. There’s a single platform, a single global dataset and a single set of forecasts that everyone in your business can collaborate on and access, based on permissions you set.

2. Open Banking APIs

But of course, for that data to be useful, it needs to be accurate.

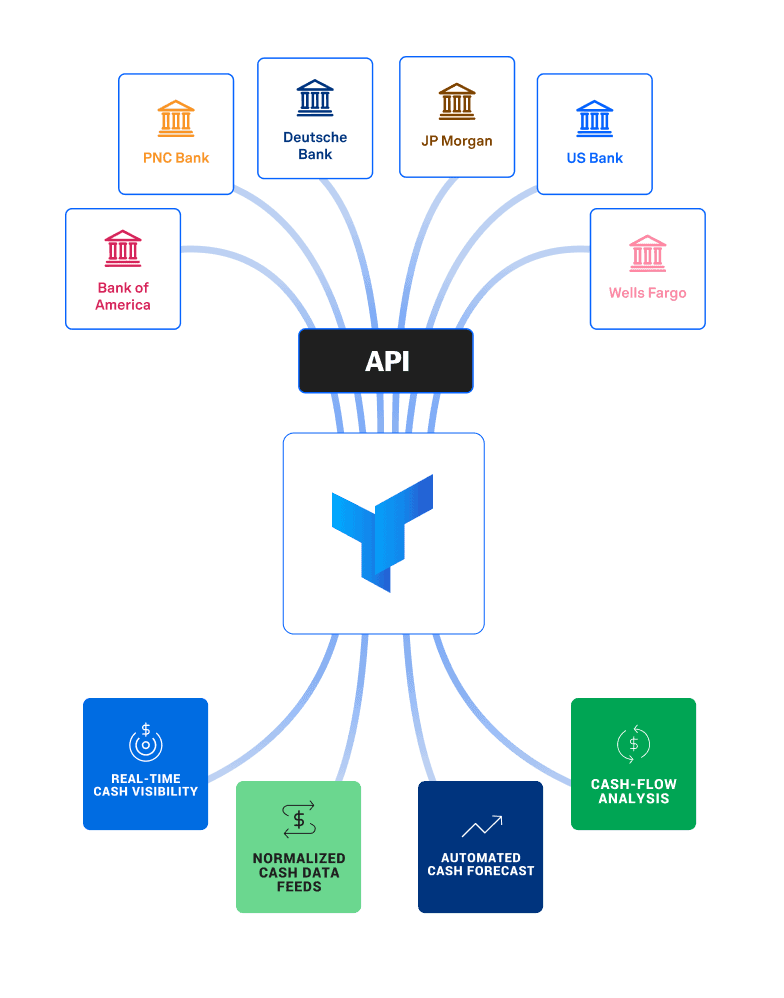

For this reason, cloud native technology pairs up beautifully with open banking APIs, giving treasurers a direct, consolidated banking data feed that can be accessed from anywhere.

The typical cash consolidation process is highly manual. Your employees would login to each banking portal individually, export a .csv file and consolidate all of this data into a master spreadsheet to provide the overall cash position.

This process could involve hundreds of individual accounts and take multiple hours each week. And because the whole process takes so long, by the time the data has been sent, it’s already out of date.

Open banking changes all that, giving companies the ability to link their financial data from multiple different financial institutions straight into an external platform like Trovata. This creates a mirror of the financial data from your bank and onto the platform, meaning that it is always 100% accurate, always real time, and free from risks like transcription or formula errors that are so common in spreadsheets.

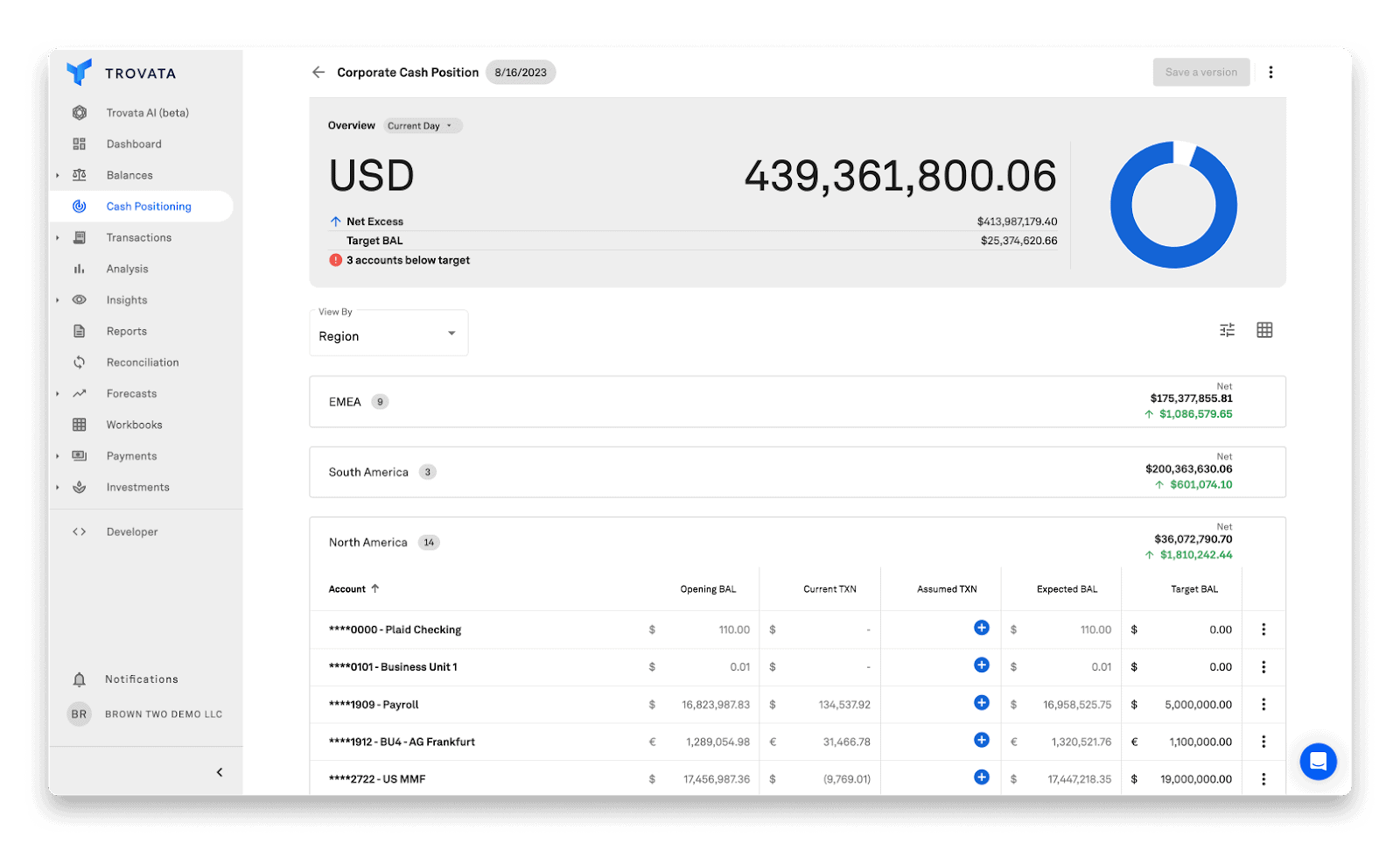

Trovata offers a single dashboard view of the entire company cash position, ensuring that treasurers and other senior executives are basing their strategic decisions on data they know is accurate and current.

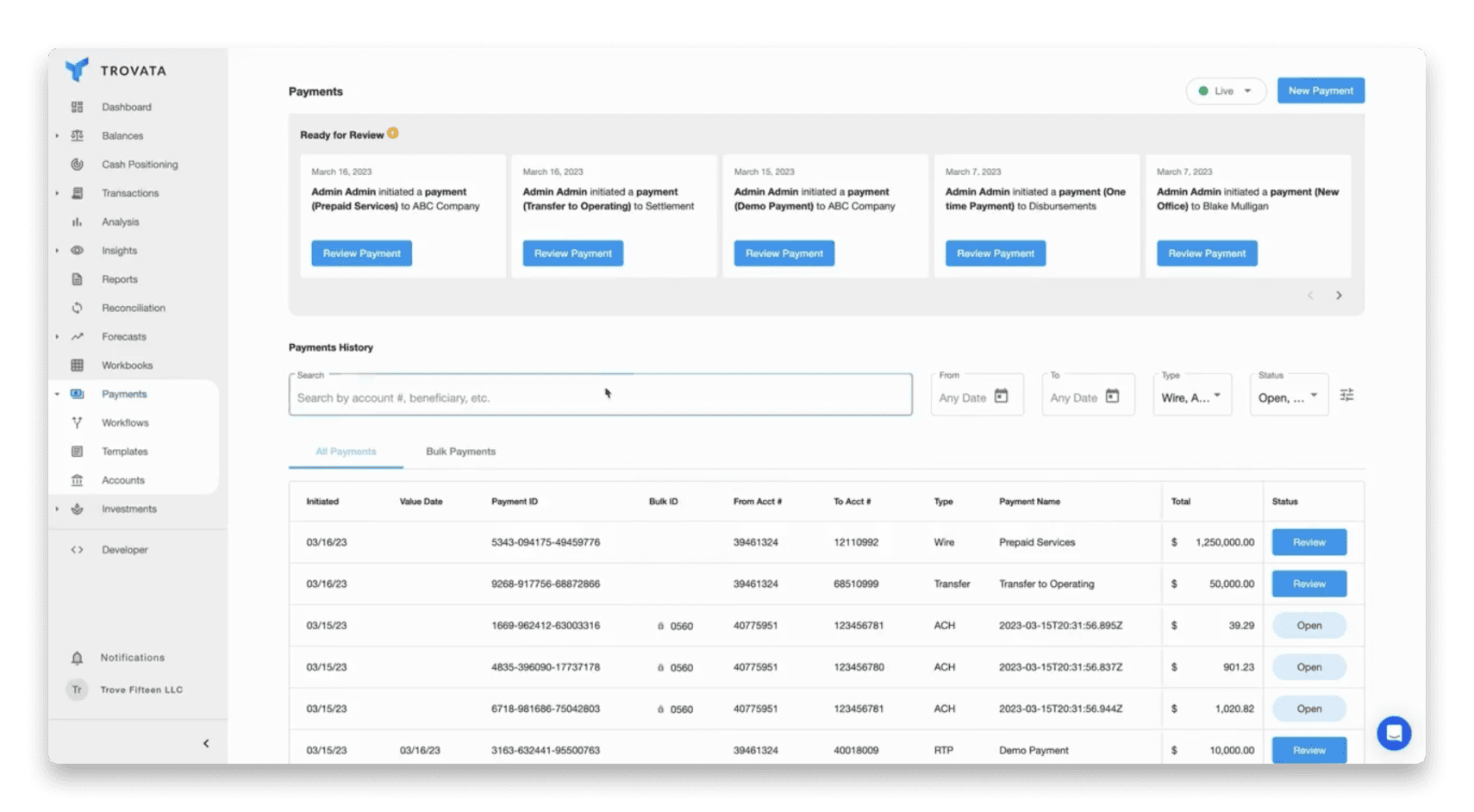

Using the same technology, treasurers are also able to streamline their payments process. For insurance companies with countless claims being paid out and constantly reviewed, having a single consolidated payments platform could be a complete game changer.

Trovata’s payments feature provides a single dashboard to manage all of your outbound payments. This substantially cuts down on time spent manually initiating payments from multiple portals, and improves security by limiting access to your banking credentials.

3. AI

Cloud based platforms and open banking provides your business with a foundation of accurate and real time corporate financial data. But accurate data is just the first part. Being able to find and access it in a way that’s usable and actionable is just as important.

Generative AI has made huge steps in the capabilities of doing just that, with tools like Trovata AI allows users to ‘interrogate’ in just about any way imaginable.

It gives treasurers the ability to create cash flow scenarios on almost anything, in a matter of minutes, using natural language prompts. This provides substantial value against a backdrop of the challenges we’ve outlined, and means even the most junior members of your treasury team can run sophisticated financial analysis.

For your more experienced members of staff, that means less time spent building the financial models, and more time interpreting and providing strategic advice on their results.

Trovata AI helps with historical data too, allowing you to search and find transactions, identify trends and find reasons for anomalies in your data. All of this can be done simply by interacting with the natural language chatbot, meaning a straightforward learning curve and no complex data manipulation formulas or strategies.

Simplify Insurance Treasury Management with Trovata

One of the most time consuming and frustrating components of treasury management for insurance companies is the bank reconciliation process. The complex web of payments, premiums, refunds and more, makes for a migraine-inducing number of line items to be consolidated.

The traditional bank reconciliation process involves a huge amount of human intervention and time, which also introduces substantial opportunities for errors. With Trovata, almost this entire process can be automated.

As we’ve discussed, Trovata integrates directly with your banking portals through the use of open banking, meaning it has a completed list of every transaction which comes through your accounts.

The platform can then be linked with your accounting software to provide a bridge between the payments that should be coming in and out, and the funds that are actually coming in and out.

This means that the vast majority of your transactions can be automatically reconciled. That’s already a big win, but as you well know, life (and cash management) is rarely that simple! There are always errors or discrepancies, but with Trovata’s automation and machine learning capabilities, these can be identified and solved quicker than ever.

While it’s still prudent to have a human set of eyes on the data, the use of this technology removes the bulk of the manual work involved in the bank reconciliation process. It gives treasurers data that is more accurate and up to date, and gives it to them faster.

Not only does it improve the ability for the treasury team to do their traditional role of managing the current cash position, but it also frees them up to spend more time on high value strategic advisory tasks.

In an industry like insurance, that’s the real value that’s going to drive performance into the future, offering your company a true competitive advantage.

If you’d like to see how Trovata can improve your cash visibility, bank reconciliation, financial forecasting, scenario planning and more, book a demo today.

Jason Mountford

Finance Professional

A finance professional with over 15 years in wealth management, Jason started Hedge, a content agency, to bridge the gap between great writers and great finance businesses. He is a fully qualified Financial Advisor in both the UK and Australia, and also works with many clients in the United States and the Gulf Cooperation Council. He’s worked with companies of all sizes, from the Fortune 500 to small boutique firms. As a financial commentator, Jason has appeared in FT Adviser, Bloomberg, Investors Chronicle, the Daily Mail, the Daily Express, Money Marketing and more. Outside of work, Jason enjoys spending time with his wife and 2 kids, and keeping active. He’s a keen (though slow) endurance athlete, enjoying running, cycling and triathlon.

Subscribe to our newsletter

In this blog post

Explore with AI

Subscribe to our newsletter

Other resources

View all in Payments