Blog

Best Practices for Account Reconciliation That Streamline the Entire Process

Written by Sergio.Garcia

December 22nd, 2023

It's been a rollercoaster in the business world lately. As companies navigate shifting economic landscapes, one foundational element they can't overlook is account reconciliation in bookkeeping. When done right, it ensures every cent is accounted for, clearly showing the organization's financial standing. Yet, many businesses still grapple with the tedious and error-prone manual reconciliation process. Juggling spreadsheets, bank statements, and general ledgers can quickly become a nightmare. And in an era where most leaders are pivoting towards tech to streamline operations, isn't it time we rethought how we handle our books? Dive in as we unpack the challenges of traditional reconciliation and shed light on best practices for account reconciliation. Trust us; you don’t want to miss out on these insights. Don't just keep up; stay ahead!

Understanding Account Reconciliation

Let's start with the basics. What is account reconciliation? In simple terms, it's the process of ensuring that two sets of financial records match—usually, this means comparing your internal accounting records to external statements, like those from a bank or credit card company.

Account reconciliation plays a pivotal role in the financial world. Without it, discrepancies can go unnoticed, leading to potential financial pitfalls, misstated liabilities, or even instances of fraud. It's the process that helps maintain the integrity of a company's financial records.

And its relevance? Think of balance sheets, general ledgers, and financial statements as the heart, veins, and lifeblood of an organization's financial system. Account reconciliation ensures the heart beats steadily, the veins are unclogged, and the lifeblood flows freely, providing a clear and accurate snapshot of a company's financial health. Without it, stakeholders, from business owners to investors, could look at distorted figures, undermining informed business decisions. Account reconciliation is the unsung hero, keeping the financial narrative straight and trustworthy.

The Traditional Account Reconciliation Process

The traditional method of account reconciliation is a trip down memory lane for many, reminiscent of a time when most tasks in the financial world were handled manually. Let's break it down step by step.

Gathering Financial Records

Initially, all necessary financial statements, bank accounts, credit card statements, and accounting records are collected. This often involves pulling physical documents or downloading multiple files.

Comparing Line Items

Next, each line item from the internal accounting system is compared with the corresponding item on the external statement, such as a bank statement. This is done to identify any differences in amounts or transactions appearing on one set of records but not the other.

Identifying Discrepancies

Discrepancies between the two sets of records are noted down. These could arise from missing transactions, incorrect entries, or simple human errors during data entry.

Making Adjustments

Once discrepancies are identified, journal entries may be made to correct errors or account for transactions that haven't been recorded yet. This ensures that the general ledger account matches the external statement.

Documentation

For the sake of transparency and audit trails, all findings, corrections, and notes from the reconciliation process are documented. This can often mean compiling a vast array of papers or digital files.

Review & Approval

The final step usually involves a review by a supervisor or another team member, ensuring the reconciliation is done correctly before it's approved.

This process, while thorough, is undeniably time-consuming. The manual nature means hours, if not days, can be spent on reconciliation alone, especially for larger businesses with more transactions to review. And the reliance on manual checks significantly increases the risk of error. Human oversight, data entry mistakes, or even misreading numbers can lead to inaccuracies. It's clear that while the traditional method has its merits, the room for improvement, especially in efficiency and accuracy, is vast.

The Role of Automation in Account Reconciliation

In today's fast-evolving business landscape, automation has become a crucial tool, especially in traditionally manual and time-consuming tasks. Yet many businesses still rely on manual processes for financial analysis. In fact, according to Deloitte’s CFO Signals survey, over half of CFOs identified inadequate technologies and immature capabilities as primary obstacles in converting data into accurate insights. Daily account reconciliation is a prime example. By automating this process, companies can quickly compare vast amounts of financial data, ensuring that internal accounting records align perfectly with external statements.

The immediate benefit? A significant reduction in time spent on reconciliation is particularly advantageous for large organizations that handle a high volume of transactions. No longer do accounting teams need to sift through every line item manually. Automation tools can scan, compare, and highlight discrepancies quickly and accurately.

But time-saving isn't the only advantage. Automation also introduces real-time financial reporting. Having access to up-to-date financial data allows companies to respond quickly to changes, making more informed decisions on the fly. This agility can be a game-changer in a competitive market, enabling businesses to adapt and move confidently. In essence, automation in account reconciliation isn't just about efficiency—it's about equipping businesses with the tools they need to operate smarter and more proactively.

Best Practices for Account Reconciliation

Navigating the intricacies of account reconciliation requires a blend of precision, efficiency, and strategic planning. Adopting best practices can elevate the process, ensuring accuracy while minimizing the time and effort involved. Here's a closer look at some of these key practices:

1. Utilizing a Modern Treasury Management Platform

Modern treasury tech software combines the most modern, emerging solutions to create efficiencies unmatched by legacy Treasury Management Systems (TMS) that are 20 years old. Modern finance professionals need a solution with the latest and greatest in technology to keep up with the demands of their evolving responsibilities.

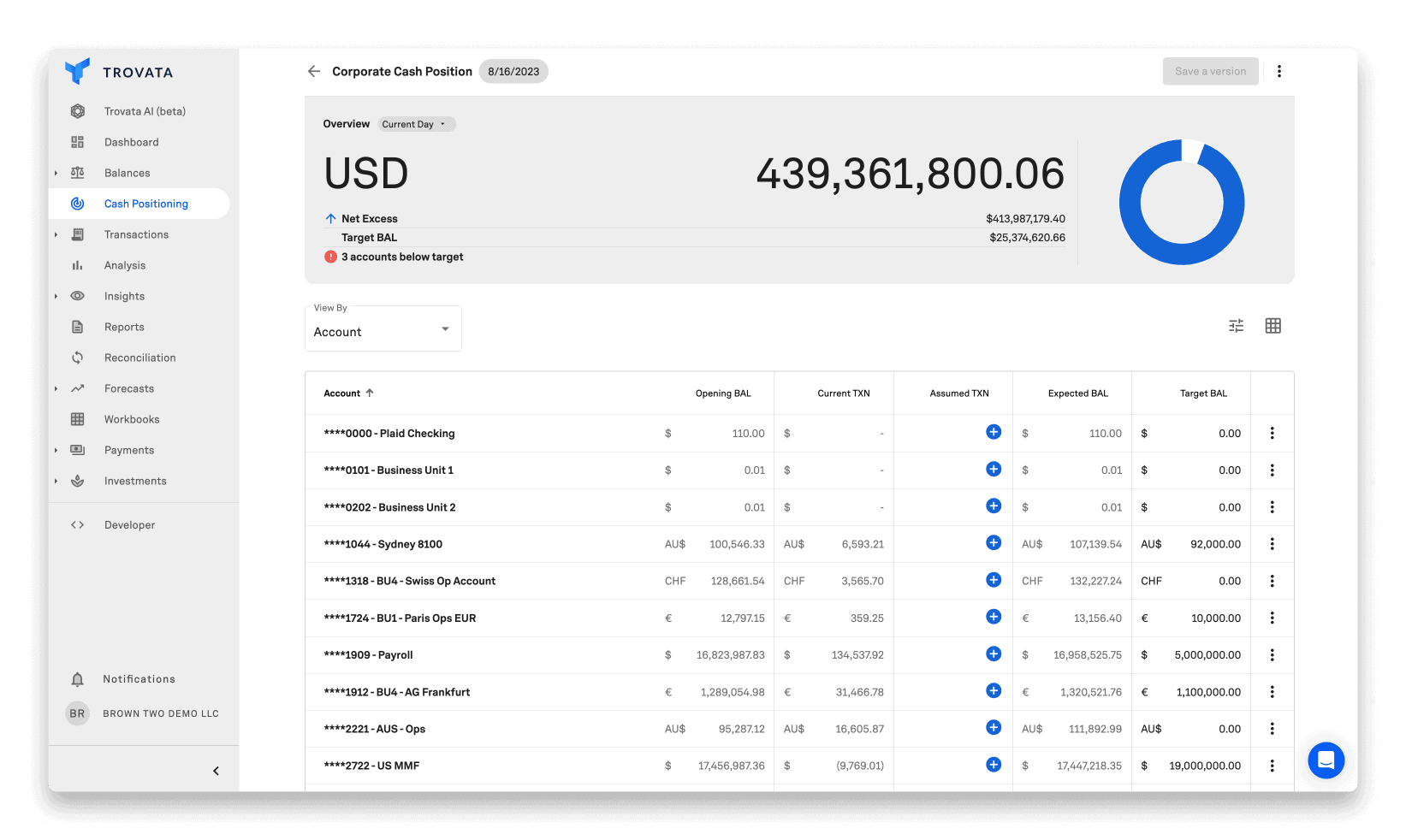

APIs

By harnessing the power of open banking APIs, companies can effortlessly link their financial data across diverse institutions to an external platform like Trovata. This integration establishes a continuous data feed, guaranteeing 100% accuracy and real-time availability of information.

Cloud-Native Technology

TMS vendors predating 2015 repackage old solutions as "cloud-based" without true native-cloud functionality. In contrast, cloud-native applications are purpose-built for public or private clouds with superior scalability and security through a microservices architecture.

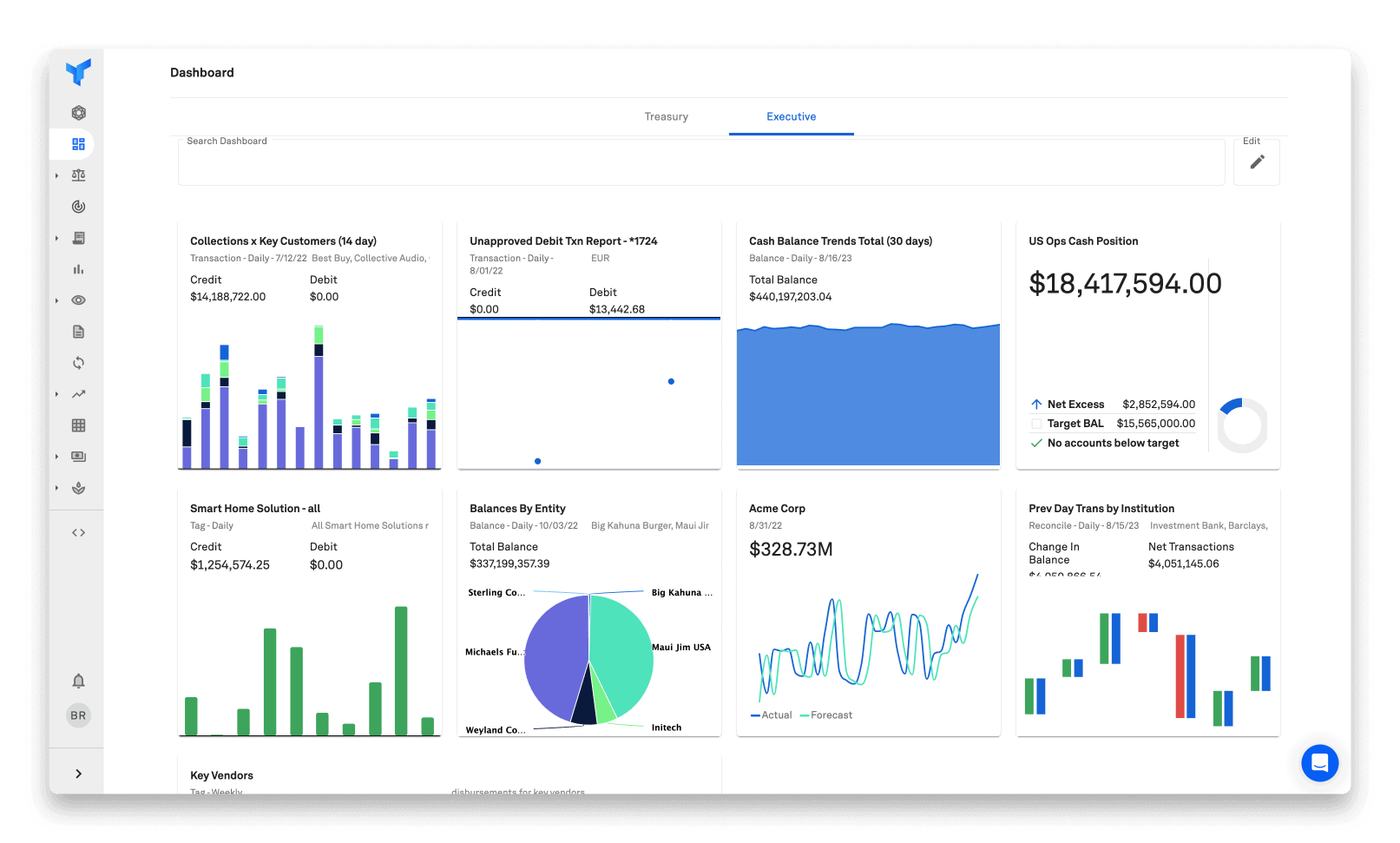

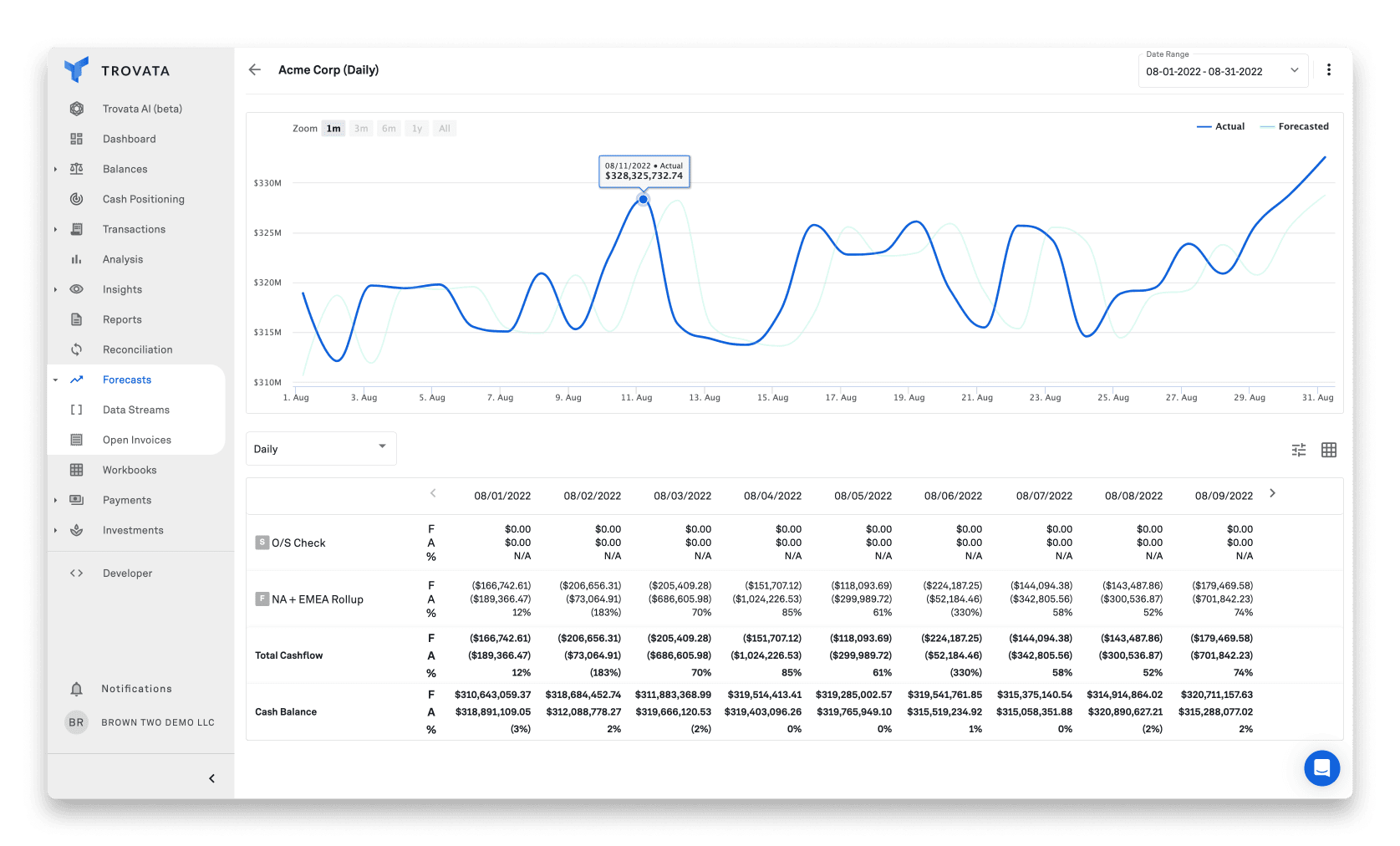

AI & Machine Learning

Modern TMS platforms automate cash flow forecasts that adapt to your organization's evolving circumstances, providing a constant, precise outlook. Historical bank account data is automatically compiled, and machine learning algorithms learn your business patterns, enhancing forecast accuracy progressively.

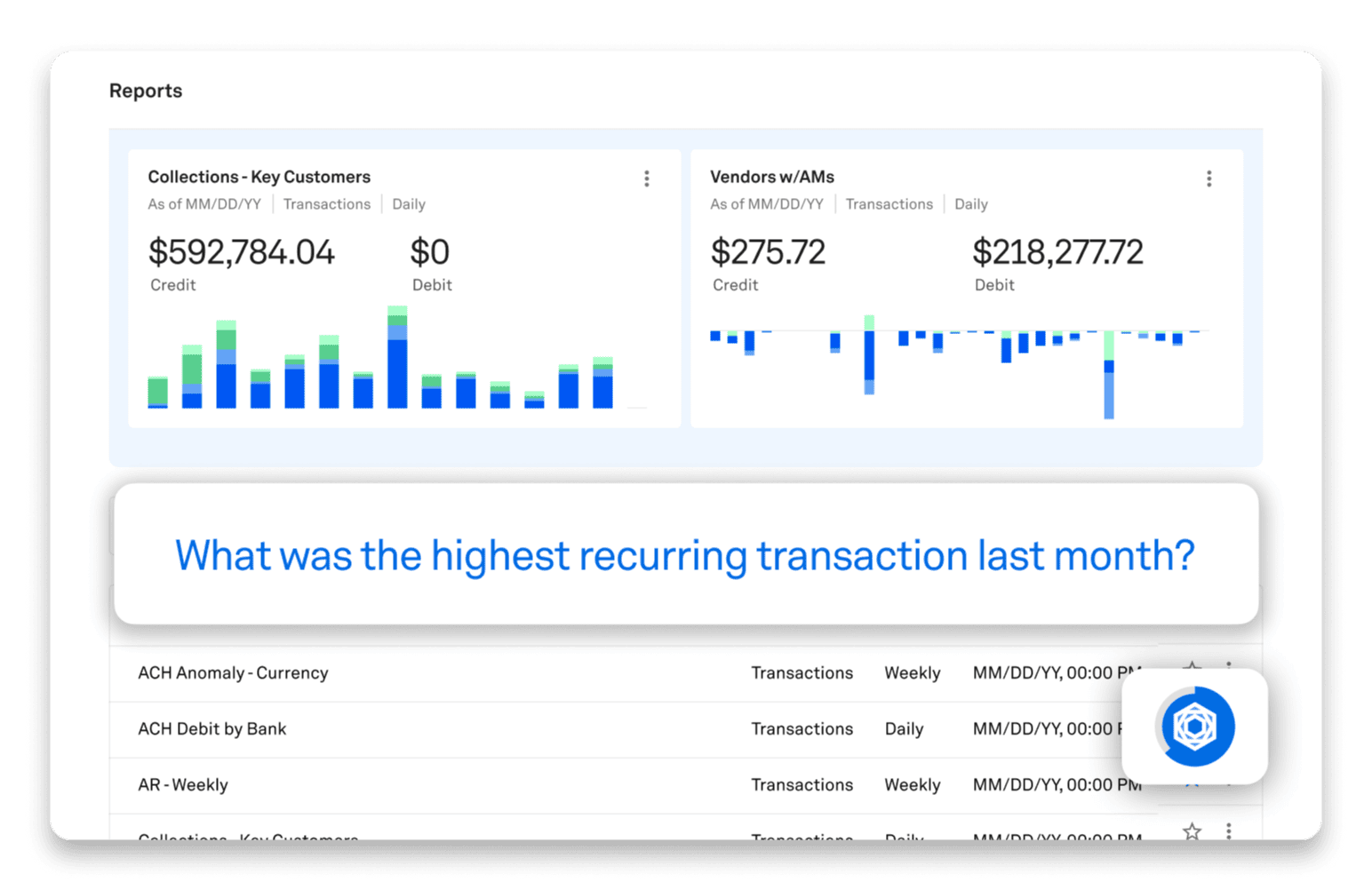

Generative AI

The introduction of ChatGPT changed the way many businesses operate, however finance and treasury pros have still been unsure of its value and use case in their functions. Trovata's platform incorporates GPT-4 technology, allowing direct, natural language interactions for treasurers. Users can ask financial-related questions without compromising data privacy. The GPT-4 language model converts inquiries into specific data requests within the Trovata system, ensuring your information remains confidential.

2. Maintaining an Audit Trail

Transparency for Stakeholders: A well-documented audit trail ensures that every transaction and adjustment is recorded and traceable. This transparency builds trust among stakeholders, ensuring they clearly understand the company's financial health.

Error Mitigation and Smooth Financial Close: A comprehensive audit trail helps in identifying and rectifying human errors. Businesses can achieve a smoother and more efficient financial close by ensuring accuracy throughout the reconciliation process.

3. Setting Thresholds

Highlighting Discrepancies: Not all discrepancies are created equal. Businesses can focus on significant variances by setting thresholds, ensuring that larger issues are addressed promptly.

Speedier Reconciliation: With thresholds in place, the reconciliation process becomes more streamlined. By prioritizing larger sets of records, accounting teams can allocate their time and resources more effectively.

4. Consistent Workflows and Templates

Streamlining the Process: Consistency is key. Standardized workflows and templates ensure that the reconciliation process follows a set pattern, minimizing deviations and potential errors.

Internal Control and Structure: A structured workflow ensures that every step in the reconciliation process is controlled and monitored. This enhances internal control mechanisms, leading to a more reliable reconciliation outcome.

5. Timely Reconciliation

Month-end Close: Reconciliation should align with specific accounting periods, most commonly the month-end close. This ensures that financial records are up-to-date and reflect the company's true financial position at the end of each month.

Maintaining Accounting Periods: Timeliness is crucial. By sticking to regular accounting periods, businesses ensure that reconciliation is a continual process, preventing any build-up of discrepancies over time.

By integrating these best practices, businesses can transform their reconciliation process, ensuring it's not only efficient but also robust and reliable.

The Financial Impact and Business Decisions

Account reconciliation might seem like a meticulous task buried deep within the accounting department, but its effects resonate throughout a business's financial landscape. Let's unpack the broader financial implications:

Firstly, accurate reconciliation impacts cash flow. Businesses gain a proper understanding of their liquidity by ensuring every transaction is accounted for. This clarity means no missed opportunities due to a misinterpretation of available funds or unexpected cash shortfalls due to overlooked expenses.

Next, consider receivables. Proper reconciliation can spotlight delayed payments or invoicing discrepancies. Addressing these issues promptly can make a considerable difference in a company's cash influx, ensuring consistent revenue streams and identifying potential areas of concern before they escalate.

Then there are expenditures. Ensuring outflows align with recorded expenses is paramount. Reconciliation helps identify any unauthorized withdrawals, duplicate payments, or other anomalies, allowing businesses to address them head-on and safeguard against potential losses.

From a decision-making standpoint, the weight of accurate reconciliation can't be overstated. CFOs and business owners thrive on accurate data. When deciding on investments, expansions, or any significant financial commitment, the precision provided by thorough reconciliation becomes invaluable. With a clear picture of financial health, risks can be assessed, and opportunities can be seized with confidence.

Embrace the Future with Trovata

In the ever-evolving landscape of business finance, staying ahead means embracing innovation. Trovata offers a cutting-edge solution to the age-old challenge of account reconciliation. By automating the process, Trovata streamlines tasks and ensures unparalleled accuracy, freeing up your team to focus on strategic initiatives. Trovata is more than just a tool with real—time insights and a user—friendly interface; it's a game-changer for businesses aiming for financial excellence. Don't let manual reconciliation hold you back. Explore what Trovata can do for your business today and step confidently into the future of finance.

Sergio.Garcia

Sergio is a seasoned marketing strategist with over a decade's worth of experience. He is the Content Marketing Manager at Trovata where he crafts engaging resources for finance and treasury professionals to navigate the complex world of liquidity management. Aside from his passion for marketing, he enjoys training in Mixed Martial Arts at his local gym in New York, binge watching the latest anime, and playing video games.

Subscribe to Newsletter

You May Be Interested In These Other Resources