Building the Treasury of the Future

Held back by legacy technology, Treasurers have found themselves relying on spreadsheets and manual processes to manage tasks that should be fast, smooth and transparent. Ready to stop living in Excel and automate processes instead? Trovata polled Treasurers from around the world to learn how experts are thinking about and planning for digital transformation at their companies – and we’re ready to share our insights. Join Brett Turner, CEO at Trovata, to gain a data-backed action plan on building a digital transformation business case for your treasury.

You will learn:

- What digital transformation is and what it means for corporate treasury

- How Treasurers answered survey questions on business priorities, their day-to-day problems, and how they are planning for the future

- Best practices to consider when building a digital transformation business case for your treasury operations

We’re joined by Brett Turner, founder and CEO at Trovata. Brett has spent his entire career in finance in both public and private high growth companies, CPA at Deloitte, controller roles, SEC reporting at Amazon, and CFO of three tech startups since 2005. Notably, he had a front row seat to the transformation of enterprise IT by AWS as a co-founder in his last startup. With that introduction, I’ll turn things over to you Brett to discuss the digital transformation happening in the treasury space. The Future of Treasury

Thanks everybody. Excited to talk about something that’s near and dear to my heart. What we’ll talk about today is the future of treasury having a front row seat to the transformation of enterprise. How modern tech is finding its way in financial services.

We have a bank first strategy because a lot of the innovation is really happening. You know, there’s been this enormous gap between ERP systems and the banks with Excel being that primary system of record and then also treasury management systems and everything in between.

What we’ll do is walk through the various aspects of this. We’ve got a few slides and we’ll go through in terms of “how is modern tech really fueling all of this or driving all of this API?” Are you hearing about that a lot? And then why does that matter? Why is that really becoming so transformative? How is that really driving and setting up the table for the next innovation wave that we’re starting into now? Democratizing Bank Data

It’s all about the data. It’s always been about the data. What is changing right now is access to the data. So new ways to get the data feed of information. It was hard to get the information before. Now, it’s becoming more accessible. It’s democratizing that data to a broader audience, which is really exciting.

You need the right technology stack or right technology platform to really be able to take advantage of that data. You hear about this concept of “data is the new oil.” Well, it depends. It’s incredibly valuable, it could be. But can you take advantage of that? Can you turn that into something that can enable automation and drive all of the streamlining of work right now?

I’ve been in the intersection of finance and accounting. Kinda been steeped in ERP systems and carving data into a data lake and democratizing that data for the rest of the business. Driving capital efficiency and managing risk and liquidity: all the things that are also important to treasury and at scale, those issues really compound. In order to really solve these problems at scale and really drive that efficiency, you have to be able to have the data and be able to have the repeatable process. Trovata obviously exists to drive this modern big data platform, to automate a lot of these workflows, and take advantage of what is becoming available from the banks.

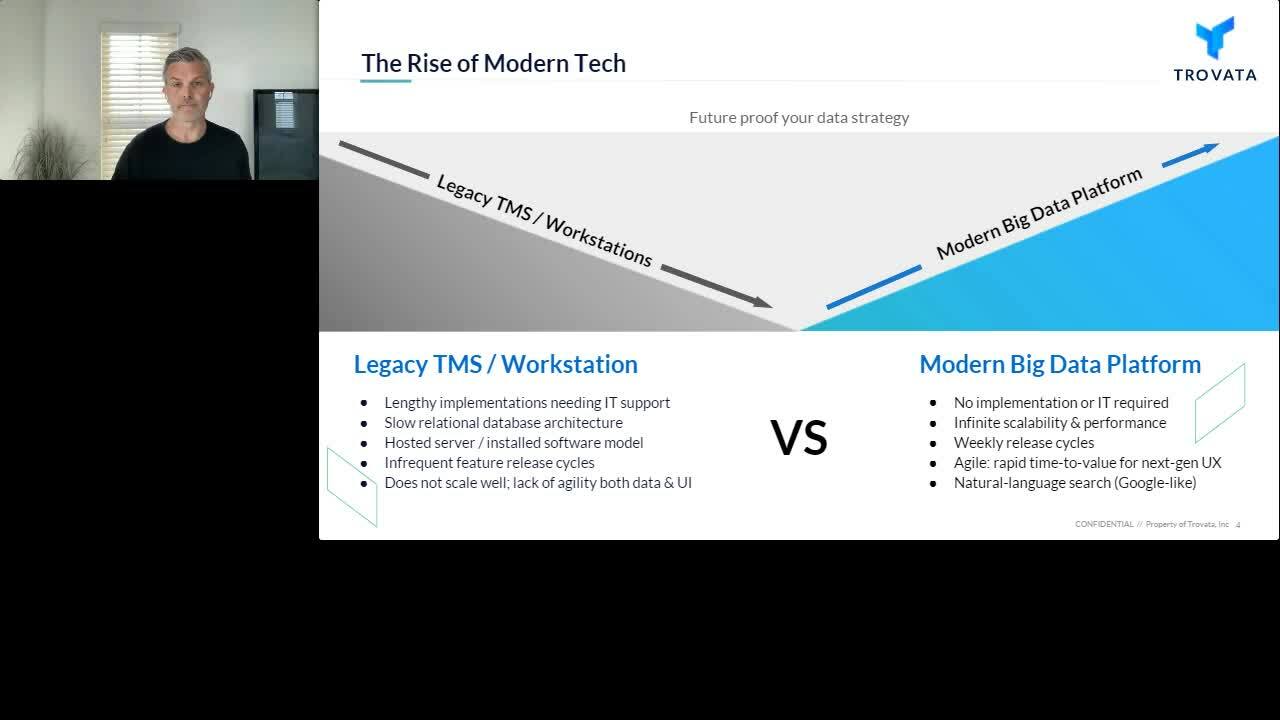

The treasury workforce is trying to streamline the TMS or treasury management systems. And with so-called workstations, even the term “workstation” sort of implies more of that legacy system. It’s kinda like the old bloomberg terminal, it’s very static and sort of monolithic. It’s really trending down.

Better Platforms Take Advantage of Bank Data to Drive Transformation

What’s trending up is the rise of more of a modern platform to take advantage of the data and drive transformation. Just like it’s happened over the last 10 years. And you look at the rise of big tech from… from Google and Facebook, really reinventing database architectures that used to be based on more relational data architectures. That whole paradigm is shifted and driven all of these modern web services where you can build natively in the cloud and take advantage of all these automated services. You can do things that you just couldn’t do previously in these monolithic, legacy structures.

What is the difference when you look at a TMS versus a modern big data platform like Trovata? One is implementation time. Why does it take a long time to connect a legacy TMS? Well, connecting to the banks is a big part of that, but also just the architecture of those systems is completely different. It’s all based on more of a relational database architecture. With the relational database architecture it’s a little bit like the old library card catalogue. If you want to find something, you have to go to the spot where that data is located. From a data query perspective, go down the aisles in that section, go down to the row, find that book. It’s the same way for data retrieval in a relational database architecture.

Problems of Scaling Treasury Management Systems

In terms of being able to scale that system, you have to be able to have a bigger database because you’ve got more transactions or more data and then you have to throw more power at it. You have to throw more compute capacity to drive through more of the requests. And therefore, if you’ve got more requests you have to throw more computing power at that.

That whole model doesn’t really align with speed and agility. Now, where you have a dynamic pipe, it’s coming in from the Bank and the API and that data feed, you can’t really take advantage of that as much as you can in a modern architecture. So that scalability or just being able to take advantage of something that’s dynamic and work all the way through a very rigid data model the UI becomes very challenging.

Contrast that with a modern big data platform and being able to spin up your instance takes seconds. And then it’s just issuing credentials, the Bank connections can still take a little bit of time depending on the API, the banks are getting faster, more dynamic. We’ll get to what will be more of an instant connection into those APIs.

In order to be able to scale, whether you’re a smaller company or a bigger company, you’re natively built in the cloud. So that cloud native architecture is really important. Maybe the question “Why couldn’t you move a legacy system into the cloud?” Well, you could, you can host it in the cloud and you can refactor a lot of your technology into an AWS. But in order to take advantage of all the agility, speed, and performance of all these advanced web services you have to be built natively. Meaning, you have to really start from the ground up. When you can start from the ground up, you can take advantage of all those components. So when there’s a new service that rolls out, you can swap it out, you know, plugging a new service in. Having that architecture allows you to be agile.

The Right Tech Stack for Automation

How can you drive automation with that data? You really need the right tech stack to take advantage of it. It’s crucial. Especially that we’ve all seen through the pandemic. Can you connect to the cloud? And maybe 10 years ago where you didn’t have a lot of bandwidth at every home. Well, obviously, we come out of the pandemic, everybody’s working from home and it was the opposite. You didn’t hear about people having problems connecting unless it was a legacy solution. You didn’t have problems. Look at the value of stock prices of all the B to B SaaS companies because of their agility, because everybody had, you know, access to broadband from their homes. They didn’t miss a beat and they actually grew because of that. A lot of that is the new era of modern tech systems and tech platforms.

Why that’s so key to be able to take advantage of APs is to take advantage of this data that’s becoming more accessible by the banks and be able to build on top of that. All of these new and advanced services will modernize and transform all the workflows bringing automation to the forefront.

Bank APIs

Let’s talk about the API. You’ve been hearing about them. So I just wanted to walk you through a bit of a timeline. This is a big part of our Trovata story. We stayed in stealth for about two and a half years building the data platform, the next Gen user experience. But it was really predicated on “Can we work with the Bank and can we get the data in a more of a direct connection from them?”

We’ve been working through this file based transmission process that’s been going on for years. It’s a more than 40 year old file format. Banks are starting to innovate. They’re moving away from that swift file based to an API. So the banks as they opened up with open banking, developing the API. They’re innovating around APIs. It’s a pass the baton sort of aspect of once they’re developing their API companies like Trovata can connect natively to those APIs, take that baton and really drive a lot of these new experiences. So that’s a big piece: the release of APIs in February 2018.

Trovata became the first to connect to those banks. And has really led now in terms of global connectivity to many banks. And it continues to build that library of direct APIs. So this is really about democratizing all of this data. Now, it’s about taking advantage of it and really transforming a lot of the workloads.

So here are some stats. We’ve done some surveying and it’s not surprising if you look at the things that we’re talking about and just being able to get time savings and efficiency gains. Really it all stems from automating, right? All these things are important but automation really is key and at the forefront of what everybody needs. Everybody’s having to constantly do with more with less, we need technology to pick up and really drive automation. And similarly, treasury needs to be more strategic. But we’ve gotta deal with all these workloads that are very clunky and manual.

Automate So We Can Focus More on the Business

It would be nice if we could automate these things so we can focus more on the business. A good aspect here at the top of the chart is having data analytics that can be more value added for the rest of the organization. Those are the aspects that are really key in treasurer’s minds today.

Then we talked a little bit about the tech stack. There are three components, the transport layer, the data from the bank balances in transactions, and then the data layer. So that big data architecture that really takes advantage of all that data can transform normalize, centralized, do all the things that are really needed to make that useful. So it can be highly available, high performance for driving things forward. Now you can do things you just couldn’t do before because you have that right staff getting the data in real time.

The API is a dynamic pipe and it’s allowing you to really change the game, allowing these workflows to be transformed. Then you look at that data architecture, being able to take advantage of it. So it’s really important that all three layers are working in concert together.

Why are we doing all this? It gets back to that staff saving time: automating work. It’s not just helping or assisting. It’s actually doing work. An API is coming in and it’s in real time and it’s updating that. Do I even have to touch it? How do we minimize those touch points so that things are being automated? Even the consumption of that data, being able to communicate that data, manage up with that data, allowing folks to access it and see reports that you’ve built so you don’t have to set up a meeting and walk somebody through it. Helping communicate that data to others throughout the organization, so they could take advantage of it and be more efficient. Let’s get that for some of these workflows, just very transformative.

Automating Reporting, Cash Forecasting

More real time cash positioning, the transaction tagging, isn’t currently in a lot of the TMSes. It’s more of this daisy chain of keywords and these if-then type table structures. With Trovata, it’s more like finding something on the internet with Google. And they’re inherently updated because the data is constantly going into those tags. These are just fundamental things that you can do with the modern architecture.

It’s allowing you to continue to make all of these things easier, automating reporting, even automating a big chunk of the cash forecasting. Cash forecasting is very hard. It’s hard to build and hard to maintain. But it becomes very doable when you have some automation to really drive the data sourcing and a lot of those pieces including from the ERP right into that system. That’s where it opens up all these possibilities.

It’s not just efficiencies for what you have. Sure we need to do that. But that’s table stakes. It opens up all these opportunities. AI and machine learning starts to kick in and alerts and notifications. Anomaly detection has come up with some of our customers as a cool feature. For transactions that are outside of the norm, you can get an alert on it so you can look at it and check it out.

Having that seamless, single sign on password is an aspect of moving between online banking and into a modern platform. All this partnership and collaboration can now start to take place in a really exciting way.

Future-proofing Your Treasury Data Strategy

A quick recap. We talked about future proofing your data strategy. Right now the innovation curve is moving. The key aspect of future proofing: the tech strategy. You’ll never be able to do certain things with the legacy conventional TMS, just from a tech architecture perspective. And so where do you value things in terms of what you wanna do as you move forward? We have major banks as investors future proofing that journey. A lot of that selection criteria is less about the classic RFP and it’s just a check across all of these features and functionality. We need to be able to open the doors of all these new things.

Knowing that there’s going to be added functionality that comes along the way, that’s a big part of the journey that we’re on with our customers, innovating in a feedback mode. We get lots of feedback from our customers. At Trovata, we’ve heard something from the customer and within 48 hours that feature is in the platform. We can do that in ways that you just can’t with the legacy TMS system. That’s what’s fueling our growth and moving very quickly as the fast growing solution in treasury right now.

Cash position, cash flow analysis, cash forecasting. We’re adding payments, we’re adding integration and automating journal entries into your ERP system. We’re on a good pace to add and continue to adopt and grow and keep up with the demands of our customers.

So we’re excited about that. Excited about the future of treasury. It’s very exciting and I just encourage all of you to really take a look at what’s out there. Think about the underpinnings of technology and bank data APIs. Transforming your workflows and behavior and how things are going to be done in the future. That can really help you move forward in an incredibly efficient way.

Looks like we have time for just a couple of questions.

“Where do you see treasurers focusing their time as they automate a lot of the manual processes they’ve been responsible for in the past?”

I’m looking, first of all, to get the right platform. How they can automate, talking to their banking team about APIs. That’s kind of table stakes of the things that we’re doing today, in automating using data to do that.

“How does Trovata’s bank API integrations different from those offered by legacy TMS platforms?”

When people ask us “If my legacy TMS has the API, how important is the API and how important is the tech platform?” Well, what happens when the bank passes a new piece of meta data through the API? How long is it gonna take to be able to adjust the legacy TMS data model and get that value? To get that piece of data all the way through the UI? It’s gonna take some time. You’ve still gotta have all the right throughput throughout the entire stack. That’s what’s key to really take advantage of the access and dynamic data via API to really get that all the way through to the user and do it quickly.”

“What are your recommendations for treasury departments with smaller budgets that are still interested in innovative technology?”

That’s one of the things that’s really gratifying for me. Because when you look at the legacy TMS the sheer cost– because it’s very linear and how they scale bigger requires more compute capacity to make it work higher and higher cost. There’s just a minimum threshold that you have to meet and therefore that minimum high cost to be able to deliver. It’s hard for some of the TMS players come down in price without taking a huge hit on their margins.

We don’t have those concerns. We can actually go and work with smaller companies because the ability to be able to flex our model in our cost of operations is just radically different. There’s definitely scale to that, we have bigger customers. But we can scale down just like we can scale up. We can meet the needs and have something that’s more in the cost of matrix that works more for the broader market and smaller companies, mid market companies. A lot of our early customers in mid market are just coming out of Excel. They’ve never really been in the treasury management systems market. They couldn’t afford a TMS. But now they can get into the game and have automation because now this is accessible too.

Speaker