Surveys suggest that 41 percent of people in the United States make New Year’s resolutions every year. However, of them, only nine percent follow through with those resolutions. Those who do, do so because they set realistic goals for themselves—and you can certainly do the same with business goals, even despite the very valid challenges that come with complicated economic conditions.

While the year 2023 has yet to unfold, predictions—rooted in the reality that inflation is still soaring, the “Great Resignation” is wreaking havoc on employment, mass layoffs are leading to low morale and so much uncertainty in the banking industry is taking a toll on consumer spending—have shifted many people’s priorities. All of the above has particularly shifted the priorities of Chief Financial Officers who are tasked with turning tough times into opportunities.

If you’re one of them, here are eight resolutions to consider for the new year to set your company up for success, based on what I’ve learned from conversations with over 100 CFOs last year.

8 Resolutions CFOs Should Consider for the New Year

These eight resolutions can help you make a greater impact in your department, in the C-suite, and in your overall business in 2023.

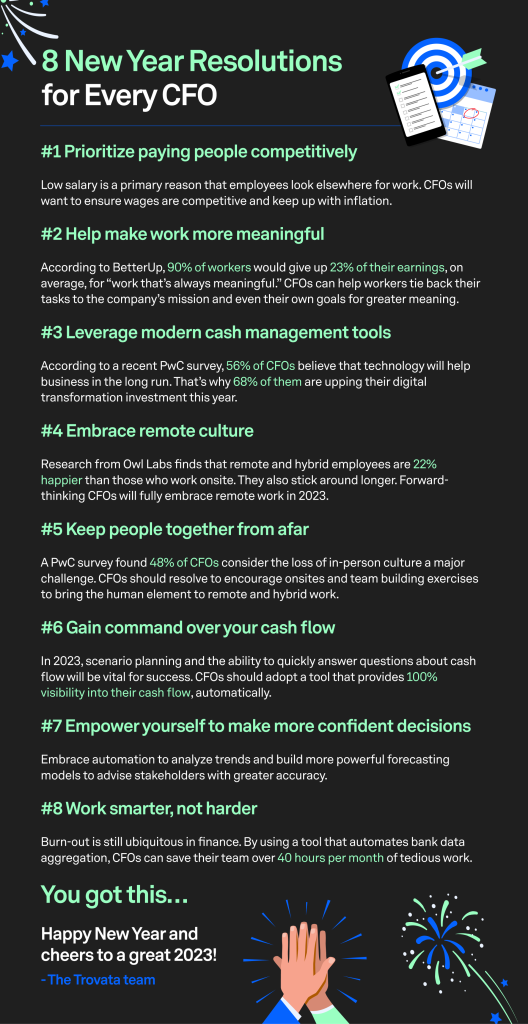

1. Prioritize Paying Your People Competitively

Research from the Pew Research Center reveals that a low salary is a primary reason that employees look elsewhere for work with bigger paychecks or better benefits. In 2021, 63 percent of people said low pay, followed by a lack of opportunities for advancement and feelings of disrespect, was why they quit.

CFOs are largely aware of this concern. A Bankrate report finds that even they can admit that “wages at their firms have not kept pace with inflation.”

“Inflation that has run at the highest levels in more than four decades has stripped buying power away from households of all walks of life,” Greg McBride, CFA, Bankrate chief financial analyst said. “Even half of those receiving a pay raise, getting a promotion, or taking on new responsibilities said that higher pay falls short of the increase in household expenses.”

While offering competitive compensation isn’t easy in an expensive economy, paying people fairly is key to retention, which is vital for success.

2. Remember That Meaning Matters

Studies show that both money and meaning are major motivators for employees, many of whom are quitting their jobs because they’re not earning enough or because they aren’t finding fulfillment in the work they’re doing.

More specifically, 66 percent of employees say that their employers’ positive impact matters even more than money. In fact, nine out of 10 workers would sacrifice 23 percent of their earnings, on average, for “work that’s always meaningful,” a recent BetterUp survey finds.

Why? McKinsey research purports that, since the COVID crisis, nearly two-thirds of U.S. employees admit to reflecting on their purposes in life—and 70 percent of them feel that their purpose is largely manifested in the work they do.

According to the Pew Research Center, jobs are among the top three most-mentioned purposeful parts of life. And, according to a recent report from Allison+Partners, 92 percent of C-suite executives agree that, beyond personal purpose, organizational purpose leads to greater success.

With regards to revenue, turnover and labor shortages are increasingly concerning for 81 percent of CFOs, according to PwC. Retention is a top priority. Ninety-five percent of C-suite executives believe that purpose is a source of pride for their employees, making it evermore important.

One way to help employees find their work meaningful is to free them from tedious tasks like entering multiple bank portals and downloading statements. By automating bank data aggregation and analysis, you can help your finance team engage in more strategic, compelling, and thoughtful work, more often.

3. Leverage Modern Cash Management Tools

The New Year is time to forgo the spreadsheets. Time spent on manual data entry—and the human errors that come with it—can be better spent elsewhere. Leveraging modern management tools can not only increase efficiency and accuracy, but it can also pave the way for innovation.

According to a recent PwC survey, 56 percent of CFOs believe that technology will help business in the long run. That’s why 68 percent of them are upping their investments in digital transformation.

Many of the tools in which CFOs are investing use artificial intelligence (AI) to sift through masses of information and insights that would otherwise take coveted time and ample effort. Plus, AI can do it all with a level of learned analysis that humans might miss. Automation capabilities also leave legroom to better allocate resources.

Trovata, for example, automates your month-end close process by aggregating, normalizing, and storing all your bank balances and transactions with a spreadsheet-like interface—without anyone having to make manual calculations in an actual spreadsheet.

“AI and analytics are boosting productivity, delivering new products and services, accentuating corporate values, addressing supply chain issues, and fueling new startups,” Harvard Business Review researchers have said.

Studies show that leading businesses invest in AI on an ongoing basis. According to IBM’s Global AI Adoption Index, the rate of global AI adoption has steadily climbed over the years to 35 percent of businesses. And, “in some industries and countries, the use of AI is practically ubiquitous,” the report suggests. Forty-four percent of organizations are working to implement AI into existing applications and processes, and your business can do the same in 2023.

4. Embrace Remote Culture

It’s no longer surprising to see just how many people are working remotely—some of whom call the four corners of their living room spaces their offices, while others are working beyond borders. In fact, 26 percent of U.S. employees are remote these days, according to Zippia statistics.

Between 2019 and 2021, amidst the heat of the pandemic, the number of people working from home tripled, according to the U.S. Census Bureau. Ladders researchers insist that remote opportunities will continue to rise through the new year, as well.

Working remotely comes with a wealth of benefits for both businesses and their employees. Employees relish in freedoms that aren’t afforded to those refined to office cubicles. Research from Owl Labs finds that remote and hybrid employees are 22 percent happier than those who work onsite; they also stick around longer. Reduced stress, enhanced focus and increased productivity are also results of remote work.

Meanwhile, businesses benefit from this increased morale, which has a domino effect on productivity and, ultimately, results. Never mind that businesses now have access to a global pool of talent. Investing in top talent around the world can increase diversity, which brings new and innovative ideas to the table.

5. Keep People Together From Afar

While there are obvious benefits to the rise in remote work, working from home or afar doesn’t come without its fair share of challenges. While many people have found a better balance of work and life, remote work burnout and loneliness are real.

Harvard research finds that the lack of face-to-face communication is taking a toll on some remote workers. PwC finds that 48 percent of CFOs consider the loss of in-person culture a major challenge. Finding ways to bring people closer—from afar—is key to recouping that company culture. But some of those ways require budget approvals.

Engagement tools like Donut for Slack bring people together online to connect over coffee, participate in watercooler topics and strengthen their working relationships. Google Meets and Zoom also have games and resources to bring people together—but it’s important to be mindful of “Zoom fatigue,” a very real byproduct of increasingly remote work environments, as well.

6. Gain Command Over Your Cash Flow

Deloitte’s Q4 2022 CFO Signals report shows that CFOs are less and less optimistic. And their biggest concerns going into 2023 are “cost management, financial performance, and growth (inorganic and organic).”

One surefire way to mitigate those concerns is by gaining command and confidence over your cash flow. Fortunately for you, there are tools to help you do just that. Trovata, for example, exists for this purpose.

Trovata offers you 100 percent visibility into your cash flow, daily, across all banks and accounts. Not only can you have full visibility over your present-day cash flow, but you can also leverage AI-powered scenario planning to plan for cash flow in the future.

This empowers you to manage liquidity, yield, and risk with powerful bank data aggregation, search, tag, and reporting capabilities. In short: Trovata helps you establish a single source of truth for all cash data—and you can implement it in just weeks without the involvement of IT.

Never mind that you can save up to 50 percent annually by switching from legacy technology providers to Trovata—which helps your cash flow even more.

7. Make More Confident Decisions

The Collins English Dictionary named “permacrisis” as the 2022 word of the year. It’s defined as “an extended period of instability and insecurity, especially one resulting from a series of catastrophic events.” And it’s something we’re all facing these days, which is crippling our capabilities to make confident decisions—especially for CFOs.

All of this uncertainty is top of mind for CFOs, according to a survey by Protiviti and NC State University’s ERM Initiative. But tools like Trovata can help CFOs be more decisive with regards to liquidity management—and that’s thanks to Trovata’s automated analysis of trends to help you build powerful forecasting models and more accurately advise stakeholders.

8. Work Smarter, Not Harder

C-suite executives, including CFOs, are rapidly burning out. That’s largely because 41 percent of financial planning and analysis (FP&A) processes are manual, taking up ten hours of work a week, according to a survey by the Financial Education and Research Foundation (FEI).

Moreover, finance teams spend an average of 14 hours a month on preparing ad hoc reports and visuals alone. Plus, it takes upwards of three months for 78 percent of companies just to plan their budgets.

Not only is that a lot of time dedicated to manual work that could be automated, but manual work errors are also cutting into those budgets that they’re so busy planning. “Error-prone manual financial reporting processes” cost U.S. businesses $7.8 billion in 2022. What’s worse, CFOs admit that the magnitude of manual work is holding them back from making strategic decisions (47 percent) and fulfilling their roles as strategic business partners (52 percent).

With platforms like Trovata, however, you can automate these tasks without any internal heavy lifting or upkeep. You can save over 40 hours monthly by automating bank data aggregation with regularly updated banking APIs.

The Bottom Line

The world is changing—and the way we do business needs to change with it. CFOs are at the helm of much of this change, with the responsibility to keep companies financially afloat amid trying times.

Gaining a competitive advantage, creating an attractive company culture, and adopting modern technology to help you adapt to changing work environments and make more informed business decisions can set you up for success.

Sticking to the eight aforementioned resolutions can help you do all of that.

Not sure where to get started? Check out Trovata’s guides, case studies and webinars for more.