Liquidity

without limits

Trovata breaks down the barriers between banks, treasury systems, and stablecoin. Get unified control over your corporate cash with AI.

Where your data becomes

your advantage

Trovata Cash

Real-time cash visibility, forecasting, reporting, and AI insights — all powered by normalized bank data. Make faster, more confident liquidity decisions without spreadsheets or portals.

Trovata TMS

A complete treasury operating system built on the same powerful data foundation. Integrate and automate workflows across cash, banking, capital markets, payments, and accounting.

Trovata Data

A fully managed data infrastructure that centralizes, normalizes, and orchestrates your bank connectivity at scale. Unlock AI, analytics, and a more intelligent, connected finance organization.

Bank Pro

A white-labeled liquidity and cash flow experience that transforms your portal into a multibank command center. Give clients real-time visibility, intuitive workflows, and AI-powered insights — all with your brand at the center.

MultiBank Connector

API-driven, normalized connectivity across global banks. Deliver real-time balances and transactions into your products for a better client experience — all without building or maintaining complex bank integrations.

Innovation starts with the right foundation

Trovata delivers clean data, reliable connectivity, and an infrastructure built for the speed and volume of today’s financial operations. That’s what makes AI, digital money movement, and real-time liquidity management possible.

Stablecoin

Instant, programmable liquidity for global movement.

AI

Intelligence powered by a unified, AI-ready data foundation.

Connectivity-as-a-Service

Self-healing, normalized bank connectivity built for scale.

Infrastructure

A cloud-native architecture engineered for speed and resilience.

Developer Portal

APIs and tools to embed, automate, and extend your cash data.

Meet our investors

Banks don’t just invest in Trovata—they partner with us to power the future of corporate banking. From direct APIs to embedded solutions, we’re driving innovation together.

Built for execution.

Designed for strategy.

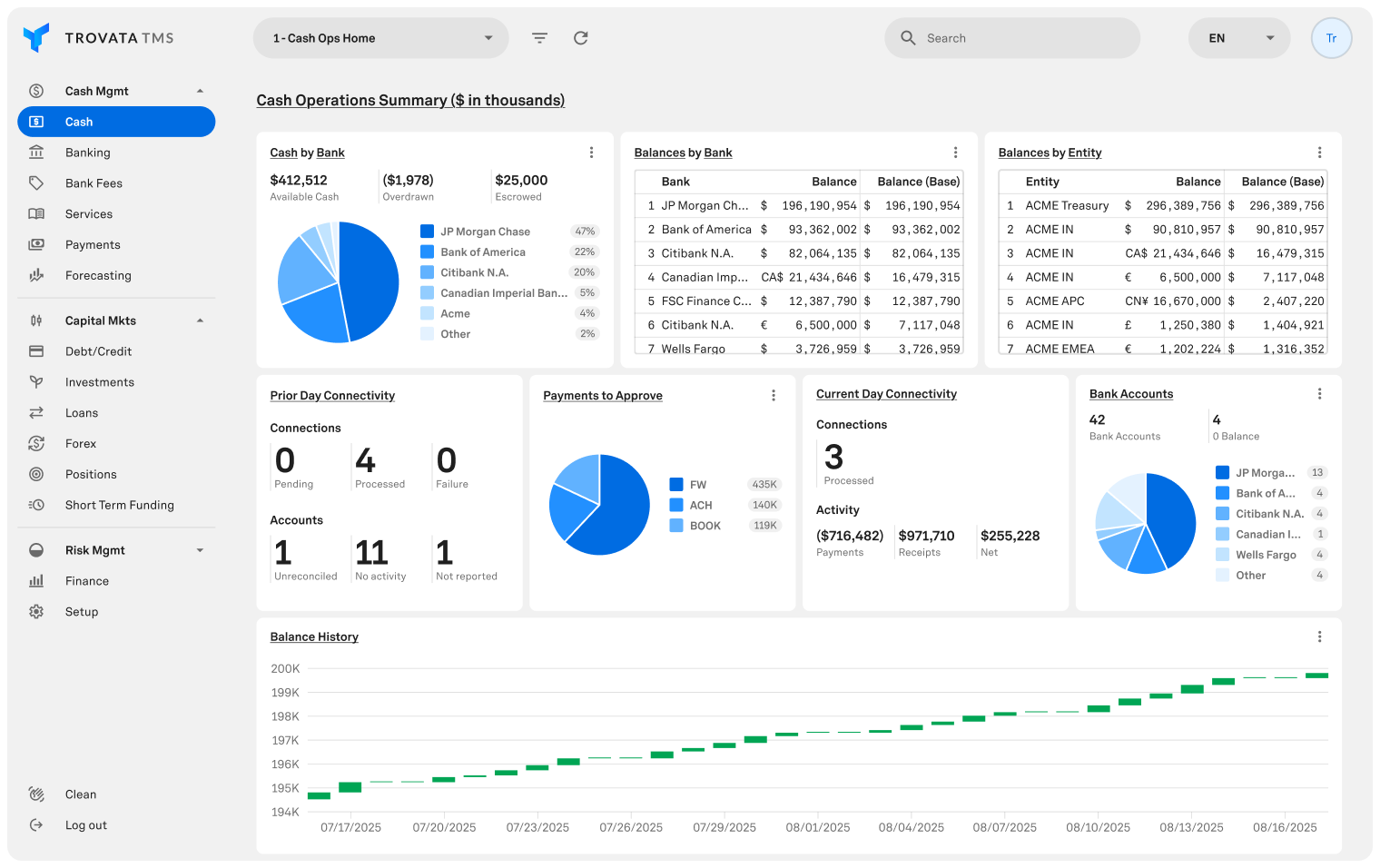

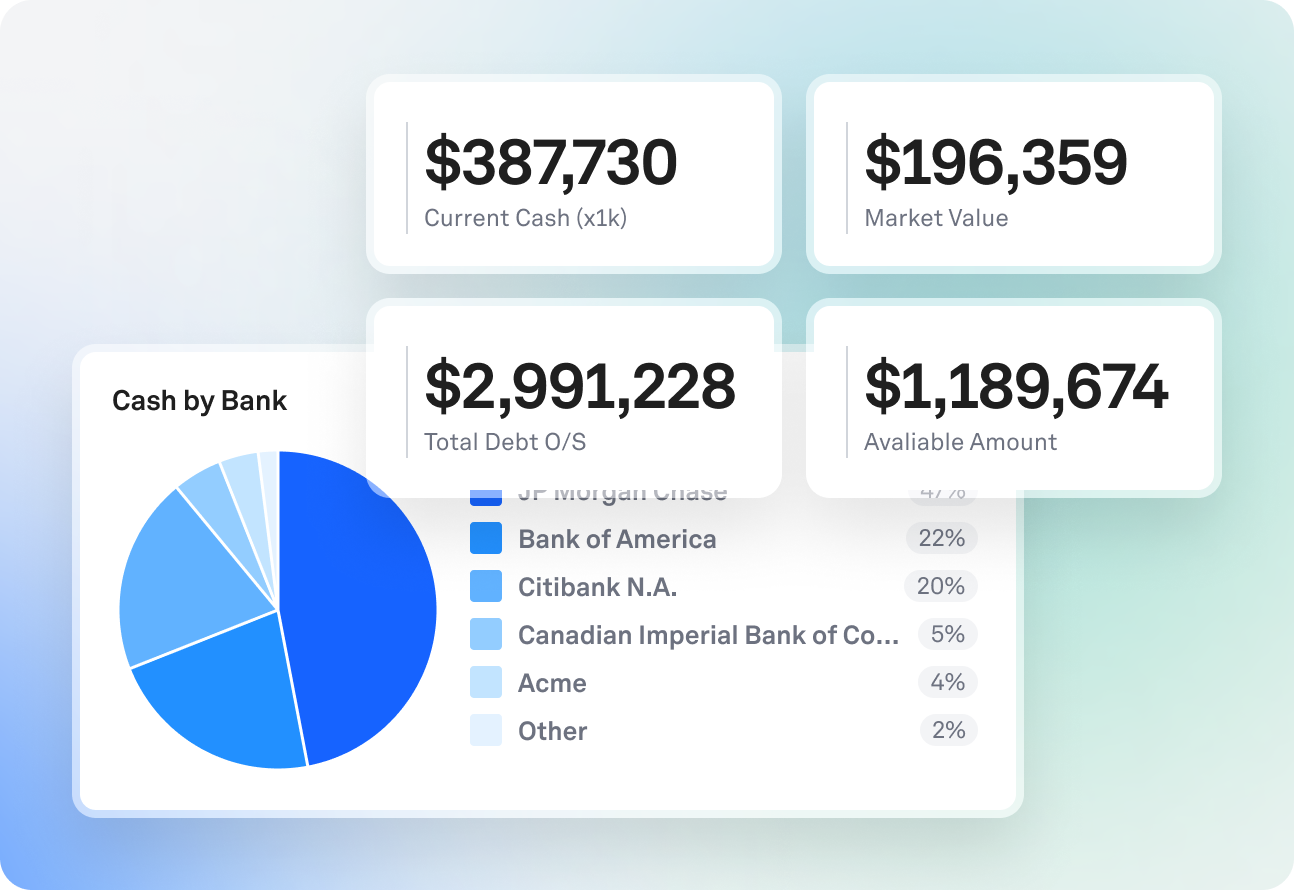

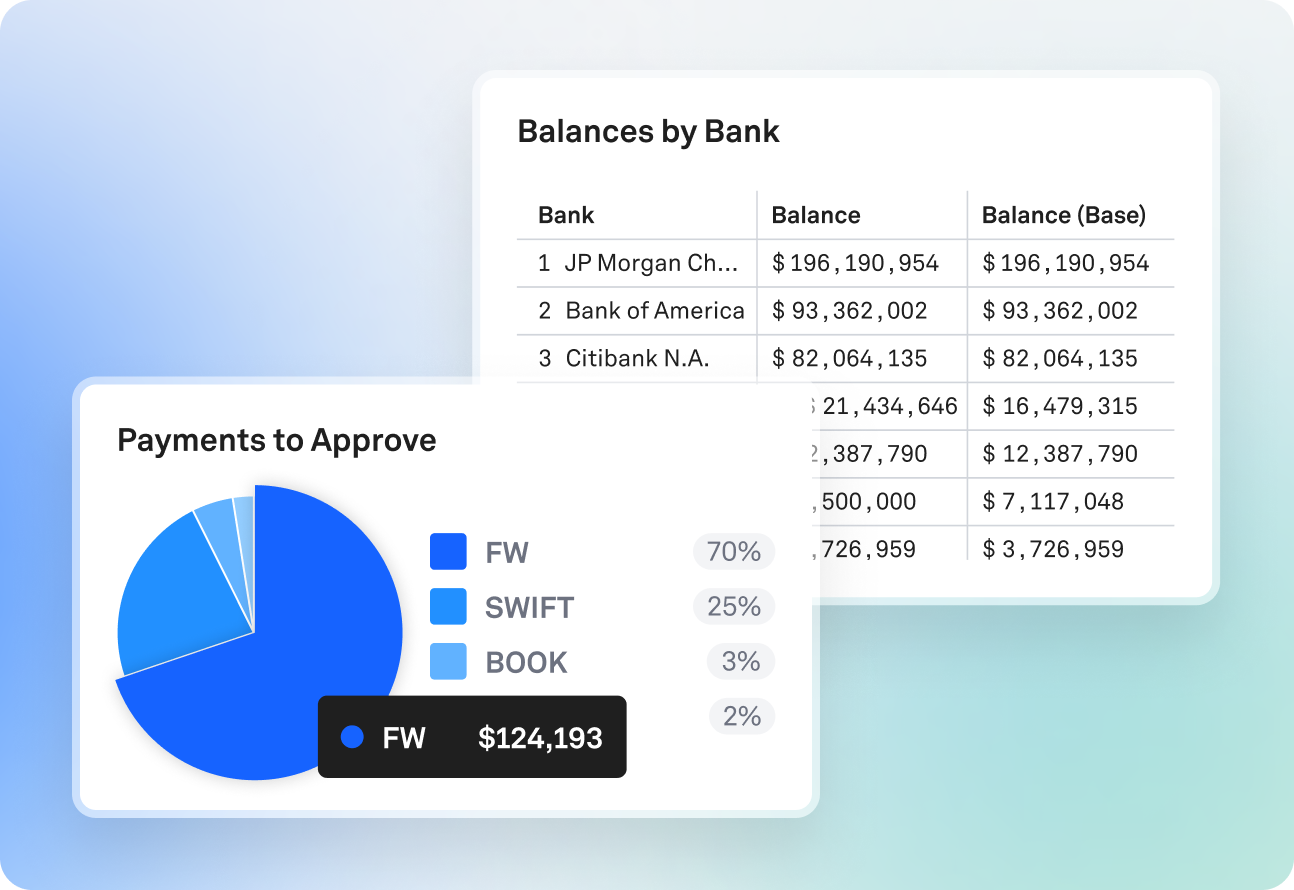

See and Control Cash

Cash reporting and positioning across banks and entities, with real-time visibility into liquidity.

Start with Cash ReportingSee also

Cash Positioning for daily liquidity decisions

Forecast Liquidity

Short and long-term cash forecasts built from historical data, ERP inputs, and projected activity.

Start with Cash Forecasting

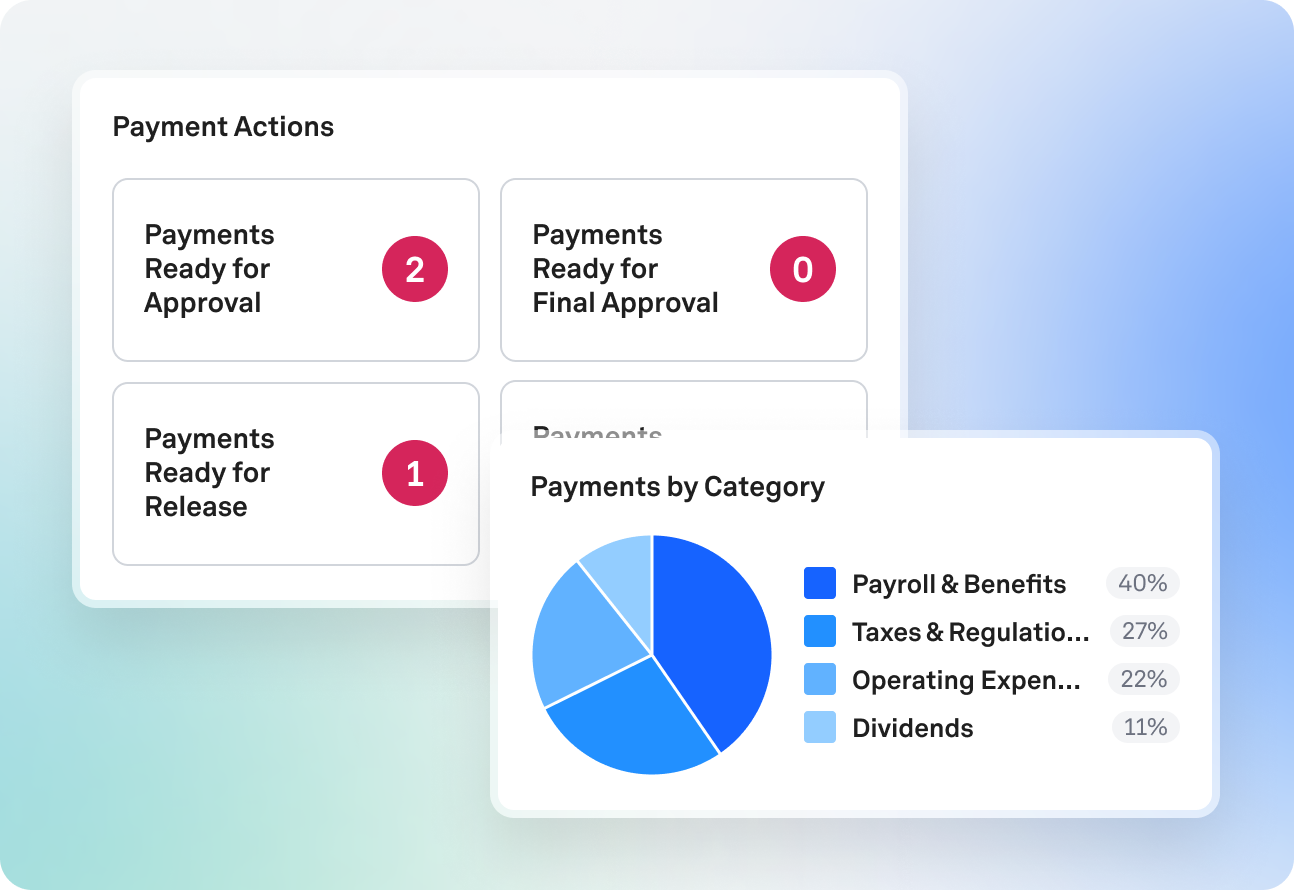

Move Money

Initiate, approve, transmit, and reconcile payments across global banks with full policy controls and audit trails.

Start with Payments

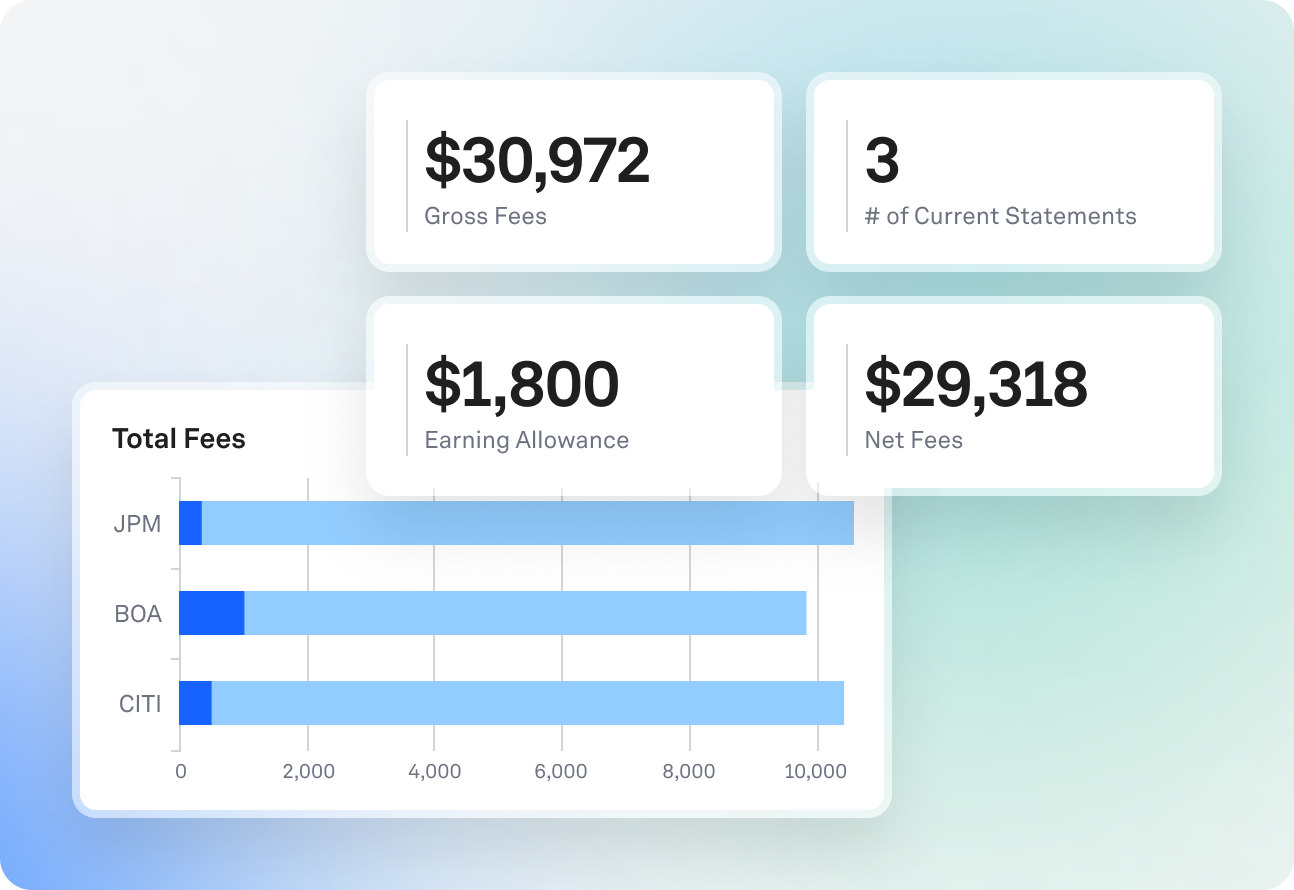

Manage Banking and Risk

Bank relationships, FX exposure, and capital markets activity centralized with lifecycle visibility and downstream impact on cash.

Start with Bank Relationship ManagementSee also

FX Management for real-time risk reporting

Capital Markets for smarter borrowing and investing

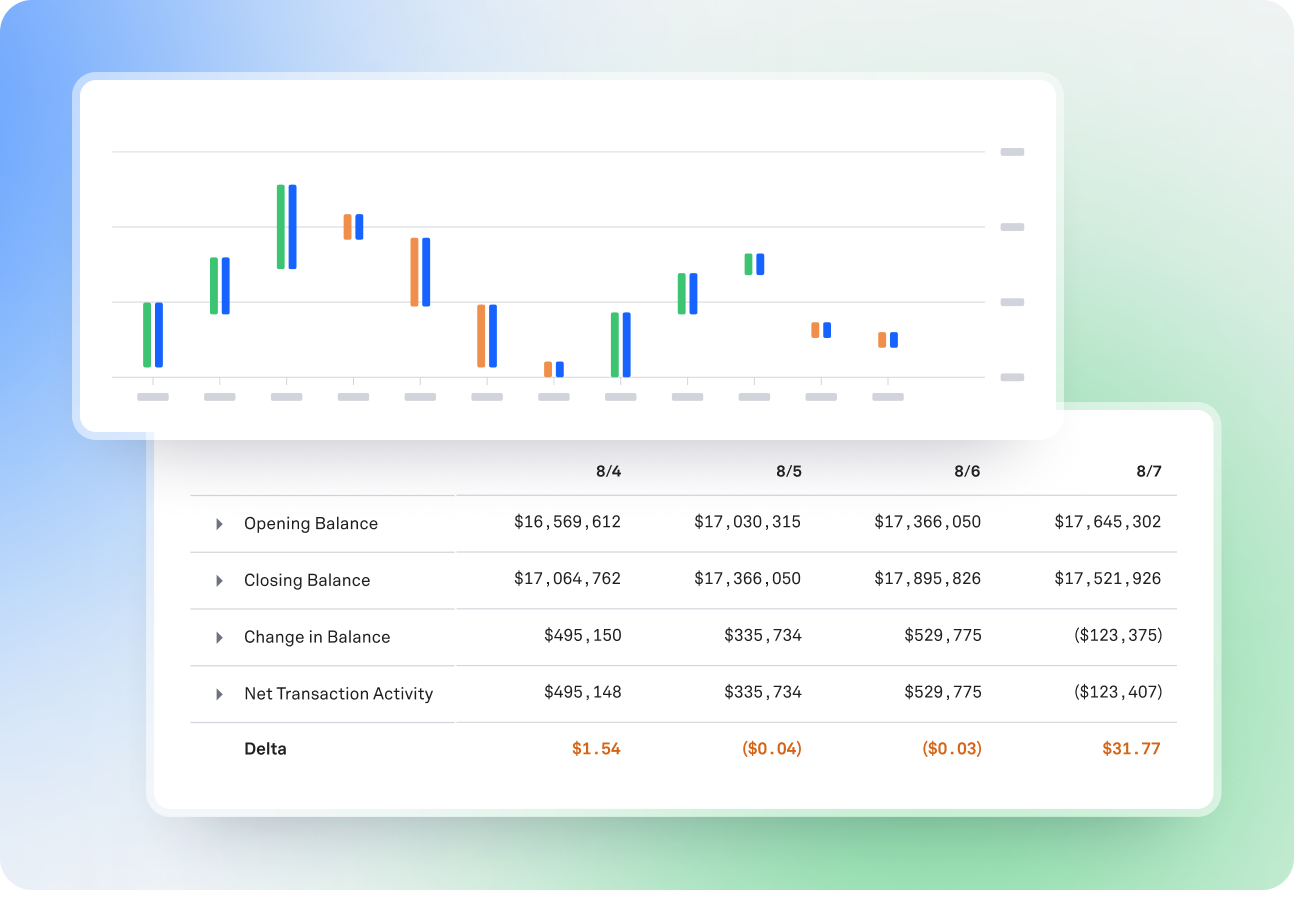

Close Faster

Reconciliation and treasury accounting workflows that produce clean, audit-ready data for your ERP.

Start with Financial Accounting

Speed and scale

you can trust

corporate deposits

bank accounts (DDAs)

payments volume

cash flow managed

daily bank transactions

You're in good company

Meet our customers

“Trovata is like having my very own employee which is incredibly valuable. It handles the heavy lifting by automating data aggregation, categorization, and reporting. Everything comes back to tags.”

Robert DiTondo

Senior Treasury Manager at Lemonade

“We started with one of our primary banks and set up an account on their developer portal, Trovata got access and the data started flowing. It took a week or two. The process was quick and super easy!”

Bruce Edlund

Assistant Treasurer at Cloud Software Group

“Eyes on our cash was our biggest problem before we had any treasury system. We were relying on monthly ERP balances and lacked access to certain international bank accounts.”

Megan McLaughlan

Treasury Manager at Park Place Technologies

Dive deeper

Visit our knowledge center

Product overviews

Access one-pagers outlining Trovata’s platform capabilities, features, and real-world use cases across treasury and finance.

Podcast

Listen to industry leaders break down real challenges, lessons learned, and strategies across finance, banking, and fintech.

Upcoming Events

Stay up to date on Trovata's upcoming in-person events, speaking sessions, and webinars.

Book Trovata Demo

Watch Recording